Best Robo Advisors

Robo-advisors revolutionized the world of investing. Let's see which robo-advisors are on top of their game.

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

Have robo advisors surpassed human advisors? 🤖

The rise of the machine-led apocalypse predicted in movies is yet to descend upon us, but “robo-advisors” have fully taken over as the go-to investment platform of the 21st century. As technology continues to upend industries, the best robo-advisor platforms have brought this disruption to the way we invest by providing services that once required a human adviser.

In a world where Siri, Alexa and other myriad manifestations of AI are household names, this was perhaps inevitable. Robo-advisors have nonetheless brought a refreshing democratization to the world of finance, birthing a new era of automated investing that hitherto never existed.

In the meantime, the growth prognosis reports for robo-advisors are quite bullish. PriceWaterhouseCoopers reports that the market is still in its infancy.

“It’s no secret that Millennials are heavily investing in ETFs and mostly via robos,” stated Nathan Richardson, an Executive Vice President of The Points Guy, as the main reason driving the growth of the robo-advisor market. However, new findings are emerging that also attribute part of this spike in growth to older clients with larger retirement savings.

This article aims to provide you with in-depth info about the best robo-advisors at the moment and help you understand why they’re so revolutionary. So, no matter if you’re a novice or an experienced investor, this article should give you some useful insights and help you choose the robo-advisor that suits your needs the best. ℹ️

Overview: Top Robo-Advisors in 2024 🤖

The automated financial advice services that robo-advisors provide have been gaining a lot of popularity in recent years because they offer a relatively uncomplicated, simple and hassle-free way for people to invest their money.

We looked at several angles while deciding which robo-advisors stood out as the cream of the crop, basing our judgement on factors such as their ability to smartly rebalance portfolios, perform tax-loss harvesting, and generally present advice that best serves their clients’ needs.

Below are our top picks for robo-advisors:

Leading Robo-Advisors

The following list presents top robo-advisors that can better your investment strategies:

The following list presents top robo-advisors that can better your investment strategies:

- Betterment

Best Overall Robo-Advisor - Wealthfront

Best for Rookie Investors - Charles Schwab

No Commission Fees - SoFi Invest

Best Educational and Investment Planning Tools - Ellevest

Best for Women Investors - Empower

Ideal for High-Net-Worth Investors - Wealthsimple

Best Socially Responsible Investment Options

1. Betterment – Best Overall

Pros

- No minimum deposits

- Easy to use and account setup is a breeze

- Costs only 0.25% annually, while offering many customized portfolios

Cons

- No margin lending or secured loans

- Frequently not-too-subtly nudged towards the funding an account.

Staying power, along with being a pioneer pays, as demonstrated by the online financial adviser, Betterment. Though Betterment was founded fairly recently (2008), its reputation is cemented as one of the foremost innovators to automate the investment process.

Rising to the forefront and staying there in the fast-paced, innovative landscape of FinTech services requires more than just offering cold algorithms. Betterment has demonstrated the ability to continually evolve, and has recently been busy consolidating customer assets by adding banking capabilities, in addition to offering retirement advice, which it views as a fiduciary responsibility.

Whether you’re a seasoned pro or a new investor, you will appreciate Betterment’s robust portfolio of features. Yet, it is still nimble enough to allow clients to change portfolio risk or switch to a different type, establish new goals and track the corresponding changes, and synch all their financial accounts together to get an overall picture of assets.

It provides clarity in its goal-setting mechanism so that the client can have an easy-to-follow process and each objective can be evaluated separately. This monitoring is enhanced by asset presenting the allocation is displayed in a ring, demarcating fixed income in shades of blue, but equities in shades of green.

Transparency 🪟

This transparency enables customers to see immediately where they are falling behind and perhaps allocate more resources to those areas. Betterment, in essence, helps clients where they are lagging behind on goals, and subsequently encourages them to put more aside. This prompt is especially helpful to young investors who might not necessarily feel the urgency of meeting long-term goals, such as retirement.

In other words, though distinguished as an industry pioneer in robo-advisor services, Betterment has not rested on its laurels since it helped launch the concept of substituting human advisors with digital representatives in order to build portfolio recommendations.

Cost is a critical consideration for most investors. Before Betterment came along the scene, the only recourse that most investors had was to invest in low-cost mutual funds and exchange traded funds (ETFs) by using a cheap broker to buy individual stocks and bonds.

However, instead of picking the individual ETFs, Betterment takes away the headache and attendant complexity by picking them for you based on an asset allocation you’ve previously selected. In its investment model, only those who have at least $100,000 or more in their account can build portfolios themselves, otherwise you are compelled to choose from pre-built, professionally assembled portfolios.

However, you still decide how much of your investment you want in bonds and how much in stocks, regardless of the investment tier you belong. This customization results in Betterment creating unique portfolios for each investor, while providing assistance with tools that can help every investor decide on the best allocation of investment resources.

Because its tools are goal-oriented with streamlined strategies for taxes, it equally appeals to all stripes of investors. In this vein, it comes with two service options: Betterment Digital and Betterment Premium.

Pricing and Plans 💲

Both options come with Betterment’s tax smart technology, but Betterment Digital, its legacy application, requires no account minimum while annually charging 0.25 percent of assets under management (AUM). Betterment Premium, on the other hand, requires a 0.40% fee and $100,000 in account minimums but provides phone access that is limitless in order to connect with certified financial planners.

Moreover, it affords the opportunity to invest in one of their diverse portfolios, or provide a more tailored experience through the creation of a Flexible Portfolio. This Flexible Portfolio allows an investor to build a portfolio with custom specifications, weighted according to the client’s preferences.

Further boosting its deep set of features, Betterment added more asset classes by launching banking facilities. This cash management product helps customers by placing all their finances under one virtual roof.

Cash Reserve and Checking 💰

By added banking products in the form of its Betterment Cash Reserve and Betterment Checking thereby heralding a move towards consolidation, Betterment has demonstrated it still has the chops to impact the industry by reversing a trend already entrenched in the banking and investing arena industry for ages.

While others in the investing and banking landscape shied away from this approach, Mike Reust, Betterment’s chief technical officer counters by arguing that customers are favorably disposed towards this approach because “the appetite to consolidate and simplify is outweighing the fear of having all the eggs in one basket.”

Betterment provides old and new investors alike something to appreciate with the numerous planning tools and copious advice offered along the way. Furthermore, Betterment prominently displays its recommend portfolios before funding, providing customers the ability of choosing socially responsible options, if they so desire.

After tax returns are maximized with Betterment’s taxable accounts due its utilization of instruments like loss harvesting, plus the fact that the portfolios can be rebalanced as necessary. Another competitive advantage that Betterment brings is that providing retirement advice is woven into its DNA, benefitting those seeking such long-term instruments.

It has a goal monitoring tool is aesthetically pleasing, which makes it easy to track the progress of your investment goals, along with a prime simple, asset allocation. In addition to its website, it also has a mobile app and both are equipped with online chat capabilities.

We recommend Betterment as both a good companion for investors who are just starting out and a platform that experienced investors will still find immensely useful. Our Betterment review goes further into detail, but here are the pros and cons of Betterment:

2. Wealthfront – Best for Low Fees and New Robo-Investors

Pros

- Comes with low ETF expense ratios

- Tax-loss harvesting on a daily basis

- Provides automatic rebalancing

- With promotional link, it is free for accounts that happen to be under $5,000

Cons

- Devoid of large balance discounts.

- Because there are no fractional shares, it is possible to have money idling away in your account and not invested.

Wealthfront is among the top selection of our robo-advisors picks because of its genius in appealing to both the new and experienced investors. It provides a holistic solution that blends sound financial advice with automated investment management.

It infuses a winning combination of competitive pricing with helpful assistance with goal planning, layered with clarity in portfolio building; all wrapped around seamless account services. In the emerging tradition of many of the current crop of robo-advisors, it is blurring the line between banking and online financial services with the launch of its Wealthfront Cash Account.

Why is Wealthfront Cash Account a big deal, you ask? Well, I’m glad you did.

According to BankRate’s data, its yield of 2.24% is a whopping 20 times more than the national average which currently stands at a mere 0.1%. But it gets even better – you get to keep most of the money you make because there are no fees and unlimited free transfers apply.

For the grizzled investor, it provides sophisticated tools such as advanced tax optimization strategies. It even allows you to borrow against your portfolio as a line of credit, but on the condition that your portfolio must have amassed at least $25,000.

As the value of your portfolio grows and account balance increases, so will the benefits at your disposal, such as access to more services such as their Smart Beta program, and the ability to add individual stocks.

For the neophyte just sticking their toes into the investing waters, Wealthfront’s helpful planning tools will thrill them, just like its hands-off approach to building a diversified portfolio.

Wealthfront provides a financial tool called Path, which even to those without a Wealthfront account can have access. Path allows users to avail themselves of Wealthfront’s retirement tracking.

3. Charles Schwab Intelligent Portfolios — Best for Usability

Pros

- Abundant ETF selection

- Equipped with automatic rebalancing

- No payment of both advisory fees and commissions.

Cons

- Unusually high account minimum.

- Low default sweep rate

- Large cash allocation

- Only accounts with $50,000 or more are have tax-harvesting available

Charles Schwab is already a household name thanks to its stock brokerage and investment expertise that has made it one of the biggest investment companies in the United States.

However, with the launch of its Intelligent Portfolio robo-advisory, Charles Schwab signaled its intention to pursue with vigor the robo-adviser market. With $41 billion already in robo-advising accounts, and a whopping $3.36 trillion in assets under management, it can hardly be considered as an underdog.

At Charles Schwab, they prefer to call robo-advisors automated investment services, but semantics hardly matter when you have the clout to fundamentally impact financial services the same way the company upended the investment world by offering stock trades at a fraction of what other brokers were charging.

Somehow, Charles Schwab has also managed to rock this nascent industry with a stroke of genius – by differentiating itself with two innovative features, namely, a cash asset allocation and zero management fees.

Pricing and Plans 💸

For its online advisor service, Charles Schwab provides two options to investors: the first is its robo-advisor base service called Intelligent Portfolios. This service requires at least a $5,000 minimum investment, but charges neither advisory nor management fees.

On the other hand, an alternative online financial planning service, Intelligent Portfolios Premium, provides clients with access without limits to certified financial planners for $30 monthly fee, in addition to requiring at least a $25,000 minimum balance.

After a client rudimentarily fills out the survey forms, Charles Schwab’s takes control of the rest, deploying your funds dutifully into diversified ETF portfolios.

Since Intelligent Portfolio is fully automated, your portfolio will be allocated based on your risk profile, ranging from a ranking of conservative, moderate, and aggressive. Also, in addition to rebalancing your portfolio everyday, to further help protect your assets, tax-loss harvesting is made available on accounts that have at least $50,000.

Diversified Portfolio 💵

Because it is fee-free, both new and small-scale investors are likely to find Intelligent Portfolios quite appealing. As might be expected, its robo-advisor has the advantage of being backed by the colossal Charles Schwab family brand.

Therefore, customers can leverage the fact that Intelligent Portfolio coexists with the full-service discount brokerage firm, and take advantage of numerous investment options available through Charles Schwab investment muscle.

Charles Schwab’s backing of its robo-advisory business with its brand equity and financial expertise is already paying-off immensely for the company: during a 3-month span in 2019, its robo-advisors arm added $1 billion in assets under management (AUM).

Schwab Intelligent Portfolios AUM currently sits at $41 billion (as of June 30, 2019), second only to another robo-advisor behemoth, Vanguard Personal Advisory Service, which tops $140 billion. Incidentally, what both have in common is that they are large investment brokerage houses with ample existing clients under their roof.

In addition to building a diversified portfolio, Intelligent Portfolios is also capable of monitoring and automatically rebalancing it based on established goals.

The knock on Intelligent Portfolios, however, is that both new and small-scale investors are likely to find it a bit too pricey for comfort, especially with regard to its rather high minimum account balance and large cash allocation requirement.

However, because you’ll be operating under the Charles Schwab ecosystem, as an investor you’ll have a virtually unlimited selection of investments at your disposal. These investment options include the normally expected stocks, but also a wide range of exchange traded funds, bonds, and even mutual funds. Further in-depth info on Charles Schwab’s platform you can find in our comprehensive review.

For those who recoil at speaking to foreigners working at remote call centers to solve their local issues, Intelligent Portfolios provides 24/7 live support from U.S.-based service professionals.

4. SoFi Invest – Best for Educational Resources/Best for Goal Planning

Pros

- Comes with excellent planning tools

- Unlimited access to financial advisors

- Low fees and low account minimum

- Excellent goal-setting tools

- The wider SoFi platform provides additional services

Cons

- Slow customer service

- No tax-harvesting available

- Negligible ETF universe filled with proprietary funds.

A relative newcomer to the robo-advisor game, SoFi Automated Investing – previously called SoFi Wealth – has nevertheless left its mark by proving to be adroitly competitive and managing to beat long-established entrants in key metrics.

Established in 2011 as a student lending organization, Social Finance, Inc. (SoFi) has grown from these humble beginnings by added several financial services that address its customers’ needs. One of those are its Automated Investing platform, which is under the auspices of SoFi Wealth LLC.

Due to its antecedents, it is targets younger investors who are usually fee conscious investors because they aren’t normally flush with capital. Therefore, SoFi Wealth allows you to start an account with as little as a $1 investment.

Most of this is because SoFi Wealth is built on the principles of Modern Portfolio Theory (MPT). This theory examines how risk averse investors can be able to build portfolios that optimize an expected rate of return based upon a certain level of market risk.

This philosophical underpinnings guides its account setup where the best possible return is sought given the level of risk that the investor is willing to accept.

As a result, the profile collection consists of simple setup pages asking for basic information, and unlike other rivals, it doesn’t include inquiries such as market experience, risk tolerance, or psychological “what-if” questions. Subsequently, the systems selects an option among five model portfolios ranging from Conservative to Aggressive for the client.

Conservative and Aggressive Option 🤲

The Aggressive option is ideal for saving for short-term goals, such as a down payment for a house and weddings.

The management fees for their robo-advisor is on the house, in addition to weaving other cost-effectiveness measures into the platform by providing a simple way to start investing with a small amount of money.

With no advisory fees and unlimited access to financial advisors, SoFi Automated Investing has made a reputation for itself through excellent lending products such as mortgages and student loan refinancing, including life insurance offerings.

Its tilt towards a younger crowd is also evident with benefits that appeal to that demographic such as career counseling services, exclusive experiences and events, and discounts on other SoFi products.

Conversely, it also has something for the more experienced crowd. SoFi Automated Investing is equally suited for the long-term investor who wants to do very little of their own portfolio management, courtesy of its wide range of EFT

Other features include sophisticated investing strategies.

Although it provides access to low-cost exchange-traded funds, most of these are slim offerings constituting a small universe of proprietary funds.

If you are an active investor and/or prefer a more hands-on approach to investing, you should perhaps look elsewhere. This is mainly because the platform doesn’t allow you to trade individual stocks or choose the components that make up your investments.

Cryptocurrency disclaimer: Due to a change in compliance guidance, SoFi has decided to de-list additional cryptocurrencies on Monday, June 26th.

In addition to de-listing Dash (DASH) and Algorand (ALGO), SoFi will also be de-listing Solana (SOL), Cardano (ADA), Polygon (MATIC), Filecoin (FIL), Cosmos (ATOM), and Decentraland (MANA). They will now only support 22 cryptocurrencies.

5. Ellevest – Best for Women/Goal-Based Investing

Pros

- Manage multiple goals in a single account

- Simple and streamlined website and app

- It helps to reduce the overall tax burden

- Depending on the investor’s goals and objectives, the portfolio can be tweaked and modified to become more aggressive in reaching these goals.

Cons

- No joint accounts or trusts are allowed

- While their overall appeal to women is admirable, however, some of the implementation comes off as clumsily done with points

With its bold mantra of “Invest like a woman,” I was tempted to make a corny joke about how the name Ellevest was reverse-engineered from the word Eve or something to that effect, but my stale humor shows why I should probably stick to my day job. So I’ll simply state that Ellevest is a robo-advisor service specifically targeting women.

Levity aside, Ellevest’s goal of closing the gender money gap is backed by grim studies from bodies such as the National Institute on Retirement Security which reports that at retirement, women are 80% more likely than men to be in poverty. Therefore, this robo-advisor is providing an important and crucially needed social service.

Ellevest uses an algorithm customized for women’s life cycles, and incomes. By taking into consideration salary curves that are gender-specific and goal targets, Ellevest asserts that it can help women reach the funds required to support their longer lifespan.

Former Wall Street exec Sallie Krawcheck, who is the driving force behind the Ellevest, felt that most investing portfolios were designed primarily for men, discounting the special needs of women. As a result, the platform considers things such as gender pay gap and living longer when making recommendations.

But don’t let this demographic bias fool you; with features and pricing rivaling some of the bigger players in the robo-advisor space, Ellevest welcomes all comers has stuff that will appeal to all stripes of investors.

For instance, its financial planning incorporates something for everyone. Ellevest punches above its weight by innovation in goal-based investing, touting excellent goal-based tools coupled with low pricing.

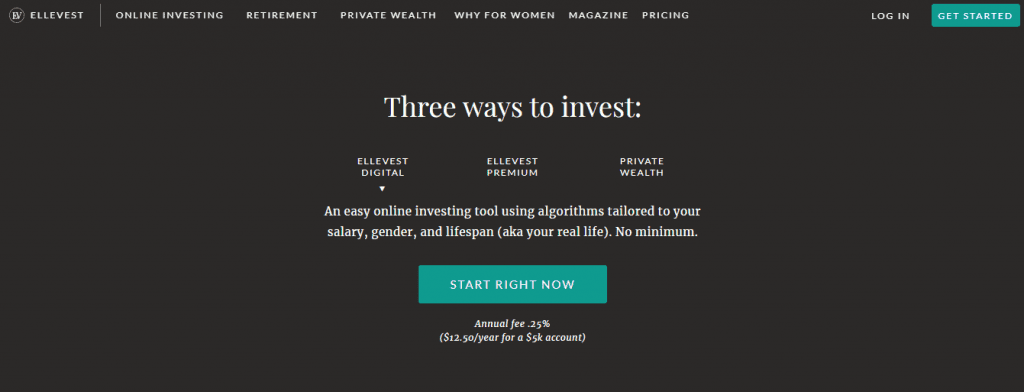

They use cutting-edge analytics to factor in disparities in pay, lifespan, career breaks caused by gender to help investors to reach their goals. In addition, to having no fees, Ellevest strives not to impose any commitments and charges no penalties for withdrawals. There a three ways to invest with Ellevest: Ellevest Digital, Ellevest Premium and Private Wealth.

Ellevest Digital 💳

If you’re just starting to invest, then this is the option you should go for. No minimum required. Provides an easy online investing tool that uses algorithms designed for your real life.

It does this by drawing your profile using characteristics such as income/salary, gender, and lifespan. These general features buttress the fact that although it is gender-centric, anyone can actually use it.

Ellevest Premium 🤑

This tier is designed for women and investors who have more resources to invest. Financial planning for people investing $50K or more. Includes all of Ellevest Digital features, in addition to one-on-one career coaching.

Ellevest Digital: At the disposal of those looking to invest $1M or more, access to a dedicated team of financial advisors providing one-on-one portfolio management for these investors.

Ellevest helps to reduce your tax burden with what it calls the Ellevest Tax Minimization Methodology. It does this by including tax-efficient muni bonds in taxable portfolios and subsequently rebalancing the portfolio in order to maximize taxable losses and minimize taxable gains whenever possible.

6. Empower – Best With a Human Touch

Pros

- High quality investment management tools

- Availability of dedicated financial advisors

- Sophisticated tax optimization strategy

- Platform makes individual securities available

- Tax optimization methods included

Cons

- High management fee

- Very expensive for most investors since it requires an account minimum of $100,000

There is no getting around it, so we might as well give it to you direct: Empower is ideal for high-net-worth investors, so if you don’t fit the bill you might need to look elsewhere for your robo-advisor needs. However, it comes packaged with a slew of financial and investment planning tools, some of which are even free to non-customers.

But frankly, one of the things that makes the platform a bit pricier than other robo-advisors because you are paying for a human financial service as well, which rarely comes cheap.

Empower can be summarized as two robust services combined into one. When you start with the free financial tracking tool, you gain access to a personal finance management platform that allows you to monitor not only your spending but also your bank, credit card and investment accounts, all in a single place.

Retirement Planner 🪙

Another gratis services also provided includes one of the most comprehensive calculators in the financial market in its free Retirement Planner.

However, when you sign up for its more robust financial management product, you’ll be provided with a hybrid robo-human advisor experience. The access to human financial advisors is a welcome development to those investors who are a bit less comfortable with handing everything over to the computer.

However, this privilege doesn’t come cheap: a minimum investment of $100,000 is required plus account balances of at least $200,000 in order to be assigned two dedicated financial advisors. (Those below this cadre have access to a team of advisors instead.)

The type of services an investor gets depends on their portfolio size. Portfolios up to $1 million are charged 0.89% per year. Fees go down for portfolios over $1 million, but that isn’t all that common for typical investors.

For most investors, these costs are really exorbitant but the paid financial advisory service, which provides a combination of computer-generated advice of a typical robo-advisor, in addition to personal consultations that have a team of dedicated human advisors, .

Checking out Empower represents a net win because even if you don’t sign up for the advising service, the Personal Capital free investment and finance management tools are still immensely valuable and worth a look as it supplies.

Empower provides investors with the ability to link existing accounts, thereby making it convenient to track net worth, portfolio performance, retirement progress and fees, as depicted below.

Pricing and Plans 💴

Empower has a three tiered investment service and it comes as no surprise that these services are delineated by the amount in assets.

- Investors with $100,000 to $200,000 in assets: The hallmark of Empower strategy is to use Smart Weighting, which spreads all investments equally across all sectors, as opposed to mimicking an index like the S&P 500. In addition these are invested in tax efficient portfolios of exchange-traded funds (ETFs) that carry a weighted average expense ratio of 0.08%

- Investors with $100,000 to $200,000 in assets: These class of investors received all the aforementioned benefits above, in addition to the privilege to customize a portfolio to include ETFs and individual stocks.

- Investors with between $1 million or more in assets: All the above apply in addition to the ability to customize a portfolio with investment in individual bond picks.

In summary, the entirety of Empower’s approach provides a personal, holistic view of a customers’ financial picture which is quite well rounded because it does not only focus on the assets it manages.

In addition, the company makes some very lofty assertions, stating that its portfolio management strategy reduces risk while also increasing returns. Empower pros and cons are listed below, but we’ve also completed a more in-depth Empower review here.

7. Wealthsimple – Best for Socially Responsible Investing

Pros

- Provides to human advisors

- Offers socially responsible investment options

- No account minimum

Cons

- Personal finance tools are quite limited

- No goal setting feature provided

- Account management fees that are quite high

Who says you can’t mix business with pleasure – or in this case with socially responsible investing. While investing and money making is serious business, Wealthsimple also enables you to feel good about your financial endeavors.

Wealthsimple, founded in 2014, is currently the largest robo-advisor in Canada and opened its business to US clients on Jan. 31, 2017. It also provides accounts those residing in the UK.

However, this relative newcomer has already showed its serious chops by becoming an award winning FinTech company. In its relatively short existence, it has managed to assemble a team of world-class financial experts and technology talent from Silicon Valley.

Features 📓

With fees ranging from 0.50 to 0.40 percent depending on the size of your portfolio, is a solid addition to the current slate of robo-advisors currently available in the market, although a rather more expensive one.

First, it offers unfettered access to a team of financial advisors, a diverse range of portfolio choices, along with unambiguous pricing.

Second, the service offers a socially responsible investment option, which allows the investor to consider both financial return to be gained along with the environmental and social impact of the product’s or company’s action.

For those of the Muslim faith, it provides halal-compliant investing options. Essentially, this allows them to invest in companies that are in line with Islamic principles of investing.

These above enumerated features are made available to all clients, irrespective of account balance. Although it is on the pricier side of the competition, values-based investors will hopefully, deem the extra money to be worthwhile spent, while also savoring the excellent, long-term investment management provision with no account minimums.

In addition to automatic rebalancing, tax-loss harvesting, and dividend reinvesting, it offers portfolio review services which provides a free unbiased assessment of your non-Wealthsimple financial accounts. WealthSimple will look into the things such as the the tax efficiency of the account, fees you’re paying, and the portfolio allocation of any third-party accounts you have.

Free Stock Trades 💶

Wealthsimple has also made the rest of us start feeling envious of Canadians by offering them free stock trades with $0 in commissions. Available only to them, Canadian investors can now buy and sell more than 8,000 stock and ETFs on major Canadian and U.S. exchanges with the new new Wealthsimple Trade app available on both Android and iOS for free.

Like SoFi Wealth, it constructs its portfolios based on the principles of Modern Portfolio Theory (MPT), by using low-cost, index-based exchange traded funds (ETFs). Simply stated MPT, demonstrates that you can minimize risk and simultaneously maximize return by diversifying your investments.

Build Portfolios Quickly 💷

Consequently, Wealthsimple uses dividend reinvesting and automatic rebalancing to complement this MPT strategy. This strategy enables Wealthsimple to quickly build portfolios by leveraging and include thousands of individual securities, which reside through a small handful of funds.

The diversity of these portfolios are guaranteed as they are invested in a mix of stocks and bonds, both domestic and international. This enables the development of a robust portfolio that invests in thousands of different companies, spanning several major sectors.

Wealthsimple offers four different types of portfolios, including the aforementioned socially responsible investing (SRI) and Halal portfolio investing. In addition to these, there are also the basic and black portfolio.

To achieve some of these objectives, the portfolios under SRI are drawn from mainly six exchange-traded funds focusing on companies involved in enterprises such as efforts to lower carbon exposure, clean technology innovation in the developing world, and supporting gender diversity in senior leadership roles.

For most investors the high fees are likely to be a deal breaker, especially when they can find rates that are more competitive. For example, its basic fee of 0.50% is at the higher-end of the robo-advisor fee spectrum.

However, you can easily do a lot better: case in point, Wealthfront and Betterment each charge 0.25% for basic service, and Betterment current provides premium services at 0.40% annually.

Apart from the high fees that are likely to put off some investors, it provides no Goal Setting feature provided by rivals such as Betterment, Wealthfront, and Personal Capital, which would really enhance the platform.

Interested in a Wealthsimple account? We’ve negotiated to get you $10,000 managed for free over a one-year period when opening a Wealthsimple account.

What is a Robo-Advisor, and how Does it Work? 🤖

A robo-advisor is an automated investment management service that utilizes algorithms to build a portfolio based on your preferences such as financial goals, desired level of returns, and risk-tolerance.

The aura surrounding robo-advisors is very hi-tech, but in reality, getting started with them isn’t rocket science. Typically, a robo-advisor gathers information via an online survey. This survey normally includes questions concerning your financial situation and future goals.

It then weighs the personal preferences stipulated such as the individual’s financial goals, thetime horizon for achieving them, amount invested and appetite for risk against unpredictable forces like asset class performance, market conditions and volatility, and so on.

In essence, it gathers this information in order to know a bit about you and your investing goals, and then builds a personalized portfolio with a risk level and investment mix that suits each goal.

It subsequently uses the data to provide financial advice and then invests the client assets automatically. Bottom-line is that they offer a solution that takes some of the stress, frustration and high fees out of investing.

Behind the scenes, however, the robo-advisor software leverages advances in cutting-edge technology such as artificial intelligence and pattern recognition to provide a cost-effective that perform tasks ranging from automatic rebalancing to tax optimization.

While the initial robo-advisor arose from necessity as a low-fee, albeit professionally managed, diversified investment portfolio comprising of exchange-traded funds (ETFs), the model is gradually being transforming into a prototype that combines a robo-human advisor.

As the service is taking shape and getting feedback from customers, many of the solely automated investment portfolios have now begun to add access to human advisors. Examples that currently stand out in this regard are Betterment and Charles Schwab.

Why Would Anyone Need a Robo-advisor? 🧐

Writing in Robo-Advisors: A Closer Look, Melanie L. Fein lays out a compelling reason for their popularity, stating that “Robo-advisors have emerged in the marketplace as an alternative for small investors who are comfortable using Internet technology but want the reassurance of an investment adviser to guide them.”

A robo-advisor is advantageous for a myriad number of reasons.

Investing and asset allocation have traditionally required basic finance skills, which many individuals unfortunately lack. In addition, the steep fees of professional advisors have put off everyday investors. As a result, advisors are available only to high-net-worth individuals.

Since it requires little or no human interaction, robo-advisors are ideal for those who want a hands-off approach with their investment. It is also good for those who don’t have the complex financial situation that requires the direct attention and relationship with a human financial advisor.

Because this type of financial adviser is automated rather than human, it costs much less and charges lower fees, which ultimately translates to higher returns to the investor, especially in the long-term.

In addition to the low cost accrue to the individual, it is also able to take sophisticated investment strategies and make them even better due to the personalized guidance it provides with smart digital technology.

What Costs are Associated with a Robo-advisor? 💵

A report from KPMG identifies that although their business models vary, they mostly provide either one of these two options – or in some instances, a hybrid of both:

- Providing investment advice solely: By using models of asset allocation, undergirded by security security selection mainly consisting of diversified ETFs, which the robo-advisor’s algorithm has ensured there is a correspondence with to the risk profile of the investor, their time horizon and goals.

- Funds’ expense ratios: These ETFs that are invested on your behalf normally charge a fee based on your assets. These vary widely, but they are usually in the ballpark of 0.05% to 0.65%. At this rate, an investor will pay $5 to $65 if $10,000 where invested annually.

- Several others recommend portfolios consisting of diversified ETFs: in this paradigm, clients pay an asset-based fee, which is dependent on the value of the account for services provided such as periodically balancing their portfolio.

- The management fees charged usually range from 0.25% to 0.5%. As you can see, they aren’t prohibitive. Therefore, assuming you invest say $10,000, it will only cost you around $25 to $50 each year.

🧠 Keep in Mind: If anything robo-advisor related is still unclear, be sure to review our introductory guide to robo-advisors.

Conclusion 🏁

Robo-advisors exist at the sweet-spot intersection where opportunity meets innovation.

These digital wealth advisors first started by capitalizing on the cutting-edge trends in artificial intelligence, pattern recognition in data, and cognitive analytics to both democratize and propel investing to new heights.

The second impetus for the robo-advisor growth was driven via the window of opportunity presented by low-interest rates and the lack of basic financial literacy among the average individual, which makes investing in the stock market seem like a daunting proposition.

The prevailing climate of low interest rates simply means that parking your money in a savings account for a bank to babysit, or even in a CD, isn’t going to cut it anymore.

Fortunately, robo-advisors address all these concerns and more: they help you make financial decisions with confidence – by doing it on your behalf instead, while eliminating the costly fees charged by their human alter egos.

On final thoughts, who would have thought that at the turn of a new decade, it wouldn’t be the much hyped self-driving cars (that have so far flamed out so spectacularly), but the rather staid landscape of finance that would bear the torch of robotic automation.

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.