Why the Lawsuit Targeting Keith Gill Screams Hypocrisy

As double standards are applied, the legitimacy of the financial system will further drain into Decentralized Finance.

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

Contrasted against publicly visible corruption left to thrive, the class-action lawsuit against Keith Gill not only seems out of place but it represents a mockery of legal standards. Even if successfully thwarted, it could imbue a chilling effect on future retail investors.

GameStop’s Double-Edged Sword

Readers following the GameStop saga are already familiar with the state of lawsuits against Robinhood. However, the nature of GME’s short squeeze was such that it amassed losses across both sides:

- Hedge funds managers who placed the short positions against a declining video game retailer with an increasingly irrelevant business model.

- Redditors who followed the guide for the purpose of bankrupting institutional investors while saving the beleaguered brick&mortar retailer in the process.

While many retail traders who jumped on board raked in huge gains, it was inevitable that some did not. As the social media mobilization rolled on, becoming a global sensation, other onboarding traders picked the wrong timeline to enter the market. Of course, this was exacerbated by Robinhood’s abrupt decision to impose trading restrictions on GME, along with other stocks targeted by WallStreetBets and crew.

The situation led to traders everywhere ditching the previously popular stock trading app, and turning to Robinhood alternatives instead.

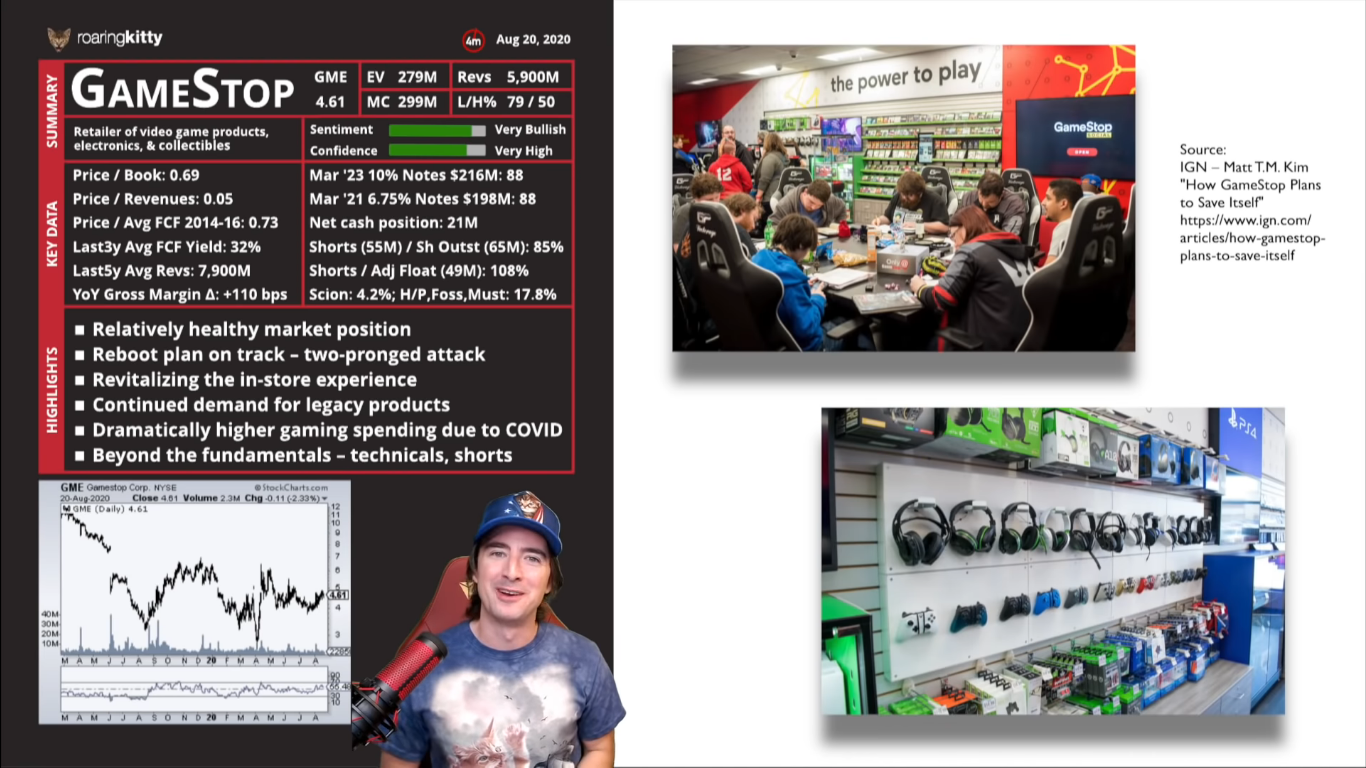

Consequently, this opened up a legal vector of attack on those who can be deemed responsible for such losses. One of the personas in the unfolding drama – “instigators” of the GME short squeeze – is Keith Patrick Gill. Known as Reddit user u/DFV (abbreviated from the more profane one), he is a prominent trader within the r/Wallstreetbets community. On August 21, he published a presentation on all the ways GameStop can buck the trend, especially in the wake of the pandemic’s social distancing mores.

Gill’s Testimony Before Congress

For his prominent role in the GameStop phenomenon, not only is Gill facing a class-action lawsuit, but he was called to testify before the House Financial Services Committee. Gill has already submitted a full testimony.

In the statement, Gill reiterates his motivation for trading GME:

“I believed the company was dramatically undervalued by the market. The prevailing analysis about GameStop’s impending doom was simply wrong.”

He then explained why GameStop’s undervaluation spurred him into action:

“First, the market was underestimating the prospects of GameStop’s legacy business and overestimating the likelihood of its going bankrupt.

…

Second, I believed – and I continue to believe – that GameStop has the potential to reinvent itself as the ultimate destination for gamers within the thriving $200 billion gaming industry.”

He concluded by stating the obvious. There were many factors responsible for some people losing and others winning. It turns out that the “free market” is a much more opaque affair than it is portrayed. One needs only to follow Robinhood’s fall from grace to come to that conclusion:

“Threshold lists, order flow, halting purchases – according to the media these all had a material impact on GameStop stock in January. Here’s the thing: I’ve had a bit of experience and even I barely understand these matters. It’s alarming how little we know about the inner-workings of the market…”

Will the Class-Action Lawsuit Against Gill Go Anywhere?

Whether this can be successfully proven in court remains to be seen, but Gill was charged for violating federal securities laws in the Massachusetts District Court, alongside MML Investors Services, LLC (“MML”), and Massachusetts Mutual Life Insurance Company. The law firm is actively seeking plaintiffs who have suffered losses.

The class-action lawsuit purports that Gill had an undue influence on his numerous followers. Steve Berman of Hagens Berman law firm handling the case, framed Gill’s involvement as follows:

“Investors from all walks of life were significantly damaged by the price manipulation incited by Keith Gill and his unsuspecting followers who hung on his every word. We are focused on what MML and Massachusetts Mutual knew about Keith Gill’s activities,”

On its face, the entanglement of Gill’s employers seems to be a fruitless endeavor. After all, Gill doesn’t have the role of a financial advisor within the company. Instead, his financial role doesn’t extend beyond the official title of “financial wellness education director”. This is akin to a personal fitness trainer/guru, but for finance.

Viewed in that light, Gill’s trading doesn’t seem to violate the regulation specifying that all registered financial analysts have to report their outside securities-related activities to their employers. Accordingly, as he didn’t offer an investment advice to his clients, all signs suggest he didn’t violate the intended purpose of the law.

Moreover, Gill has been upfront about his reasoning from the get-go in August, backing the trades with his own money. As for his undue influence on the masses, his channel’s growth spurt occurred later. Before GME heated up, he had a minuscule number of YouTube subscribers. As his Social Blade profile shows, his subscriber count only skyrocketed at the end of December/beginning of January to its current 421k figure.

Most importantly, it is peculiar that Gill was singled out for “price manipulation”. Anyone following the stock market scene knows it is a common occurrence to offer opinions on stocks. For instance, the hedge fund manager Cathy Woods suffered no lawsuits for calling out Tesla’s stock surge to $4k.

It appears that, out of countless such calls occurring daily, many of which resulting in stock prices going down or up, Gill is being offered as an example of what happens to people when they go up against Wall Street power brokers.

Codifying Double Standards

Even when giving the individual(s) who sued Gill for incurred losses their due, his YouTube channel holds prominent disclaimers, emphasizing “for educational purposes only”. Can the same be said of prominent stock personas appearing on mainstream TV channels and publications? It certainly wasn’t the case with Cathy Woods.

Moreover, one doesn’t have to look under every rock until one uncovers stock price manipulation. The pump-and-dump scheme with Eastman Kodak is a perfect example of applying such double standards. Entangled with COVID-19/Operation Warp Speed, beleaguered Kodak received a $765 million government loan via International Development Finance Corporation (IDFC).

This itself was unusual because this agency deals with foreign aid. More unusual than that, George Karfunkel, Kodak’s directors’ board member, donated $180 million worth of Kodak stocks (3 million) to a brand-new Chemdas Yisroel Congregation with no public profile, just after Kodak stocks soared in the aftermath of the announcement.

To put the cherry on the top, the IDFC director was Adam Boehler, an ex-roommate of Jared Kushner, who was put in charge of the pandemic task force. Long story short, the whole deal collapsed and is under House committees’ investigations. The end result – no wrongdoing found!

“Kodak said the company did not break any laws with its disclosure, but faulted a gift of stock by board member George Karfunkel to a charity he founded the day after the government announcement of the loan.”

Likewise, it seems no charges will be filed against multiple senators dumping stocks after their coronavirus briefings. The routine is becoming familiar – initial public outrage, followed by inquiries, followed by fading out of the public spotlight. If only there was some kind of legal system that would be applied to everyone, regardless of class and social status. It seems the work to discover such a system lies ahead of us.

Did you know that Speaker of the House, Nancy Pelosi, bought 25 Tesla call options, soon after which President Biden announced the purchase of 650,000 EVs by the federal government? Given such an atmosphere, what do you think of Gill’s lawsuit? Let us know in the comments below.

Tim Fries

Tim Fries is the cofounder of The Tokenist. He has a B. Sc. in Mechanical Engineering from the University of Michigan, and an MBA from the University of Chicago Booth School of Business. Tim served as a Senior Associate on the investment team at RW Baird's US Private Equity division, and is also the co-founder of Protective Technologies Capital, an investment firm specializing in sensing, protection and control solutions.