BTC-0.33%

Market Analysis

BTC-0.33%

Market Analysis

May CPI Data Expected to Hit 4.2% Rate Cuts Dead for 2026?

May CPI Expected at 4.2% — A 3-Year High

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

The US Bureau of Labor Statistics is set to release the May 2026 CPI data today (June 10) at 8:30 AM ET, with forecasts indicating a headline inflation rate of 4.2% year-over-year, up from 3.8% in April.

The monthly increase is expected at +0.5%, slightly down from April’s +0.6%. This rise is attributed to three months of energy-driven price increases, bringing prices to a three-year high.

Core CPI, which excludes food and energy, is projected to be +0.3% month-over-month and 2.9% year-over-year, exceeding the Fed’s 2% target. As a result, there is about a 70% chance of a 25-basis-point rate hike by year-end, with a 38% likelihood of a move as soon as September.

The headline CPI increase is largely due to a more than 50% rise in crude oil prices since the start of the Middle East conflict on February 28, 2026, further intensified by renewed hostilities on June 7.

The Oil-to-CPI Transmission Channel: How a 50% Crude Surge Pushes Headline Inflation to a 3-Year High

West Texas Intermediate crude prices have surged over 50% since the Middle East conflict began on February 28, raising concerns about supply disruptions through the Strait of Hormuz.

In April, energy prices jumped 3.8% month-over-month, contributing to over 40% of the overall CPI increase.

This trend continued into the May 2026 CPI report, where headline inflation at 4.2% was largely driven by energy costs, mirroring the situation in May 2023 during oil price escalations due to geopolitical tensions.

In contrast, core CPI, which rose 2.9% year-over-year, indicates more stable underlying price pressures, with the three-month annualized rate closer to 2%–2.5%.

However, if core readings exceed the expected monthly increase, particularly in shelter or airfares, it could complicate the Fed’s response to overall inflation.

Higher for Longer Calcified: What a 4.2% CPI Print Does to Federal Reserve Rate-Cut Expectations in 2026

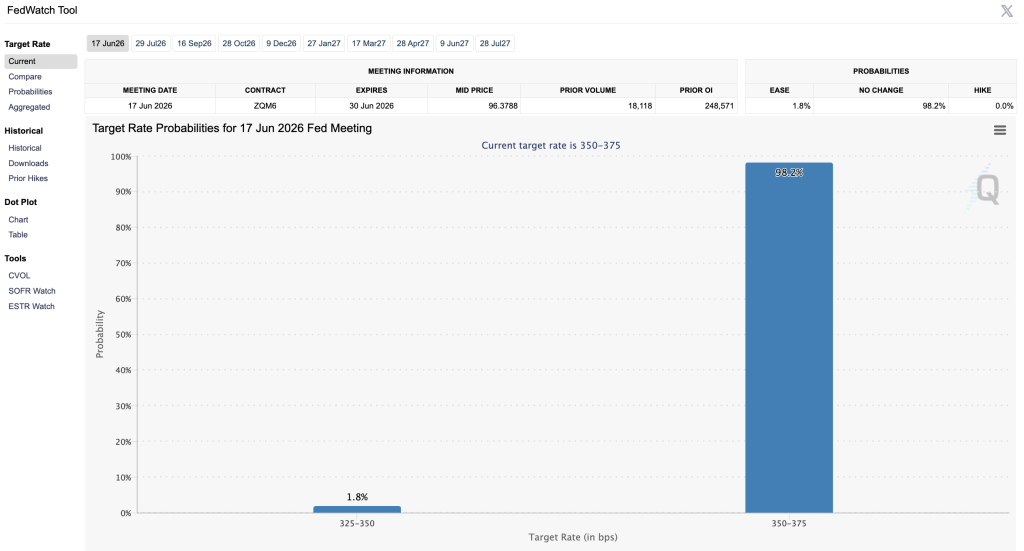

The Federal Reserve is currently leaning toward a more hawkish stance, with the CME FedWatch Tool indicating a 70% probability of at least one rate hike by year-end.

Markets have shifted away from a 2026 rate-cut narrative, with potential cuts pushed into late 2027 if inflation stays above 4%.

A May 2026 CPI reading at or above 4.2% confirms this trend, especially with strong labor market data, including May Nonfarm Payrolls rising by 172,000 against an expectation of 85,000.

The key variable to watch is the 10-year Treasury yield, which rose from 1.5% to over 4.2% in the previous cycle. A hot May CPI could push the yield toward or above 4.75%, likely affecting rate-sensitive assets.

JPMorgan notes that any Fed policy changes are unlikely before late 2026, with markets increasingly anticipating a rate hike rather than a cut, a scenario previously considered unlikely as of February 2026.

4.2% as the Dividing Line: What Each CPI Data Scenario Means for Rate Expectations and Equity Markets

In the bull case, if headline CPI is at or below 3.9% year-over-year and core is at or below 2.8% month-over-month, markets may reprice late-2026 rate cuts, sparking relief rallies in rate-sensitive equities like QQQ, IWM, and VNQ, while the 10-year Treasury yield retreats.

However, this scenario relies on a significant drop in services inflation and easing energy prices, making it low probability given high WTI levels.

In the base case, a headline CPI of 4.1%–4.3% year-over-year with core at 0.3% monthly and 2.9% annually will maintain the hawkish stance but not accelerate it.

The Fed is likely to stay on hold, leading to range-bound trading in the S&P 500 as investors weigh earnings against a higher-for-longer outlook. A 4.2% print would support this cautious approach.

In the bear case, if the headline CPI reaches 4.4% or higher and core exceeds 3.0%, rate-hike odds could exceed 70%, pushing the 10-year yield toward 5%.

This would compress valuations of long-duration growth stocks, strengthen the US dollar, and create additional pressure on interest-sensitive risk assets.

The author does not hold or have a position in any securities discussed in the article. All stock prices were quoted at the time of writing.

Tim Baker

Tim Baker is a Senior Market Analyst at Tokenist with over a decade of experience educating readers about traditional finance, crypto and DeFi. A former equity researcher turned on-chain analyst, Tim specializes in regulatory framework shifts and institutional DeFi adoption. His work focuses on distilling complex liquidity cycles and the macro environment into actionable intelligence for the modern DIY investor.