BTC+2.08%

Crypto

BTC+2.08%

Crypto

Institutional DeFi: Why Trusted Counterparty Liquidity is the Key to Adoption

Alkemi's Brian Mahoney explains DeFi's missing ingredient - and how Alkemi aims to provide it.

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

2021 has been a big year for digital assets. Core digital assets like Bitcoin caught the attention of the mainstream press (MicroStrategy & Tesla’s balance sheet allocations to name a couple) and the world has also seen Wall Street behemoths like BNY Mellon, Goldman Sachs and JP Morgan acquiesce to build out crypto research & trading infrastructure.

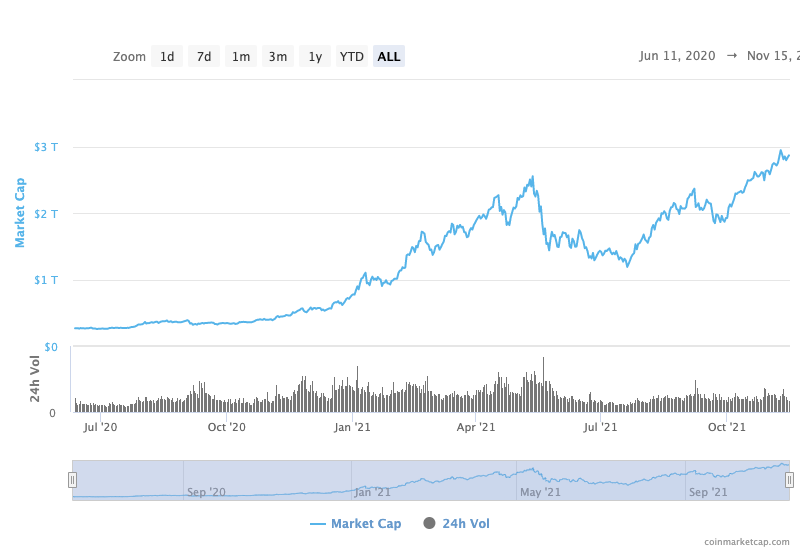

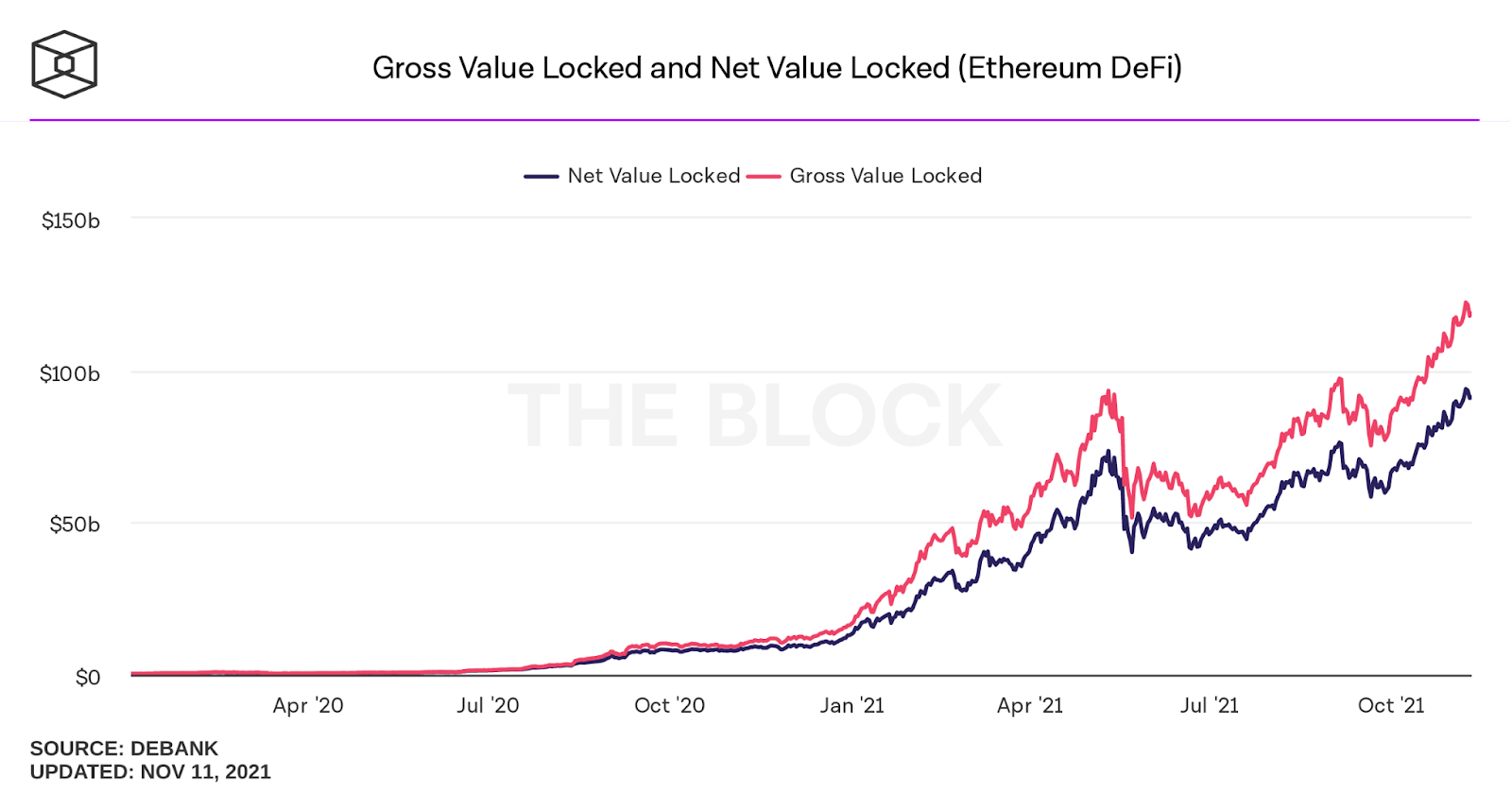

The digital asset market capitalization has soared to ~$3 trillion, a 600%+ increase YoY driven by institutions in the West and the unbanked in developing countries [Chainalysis]. Yet the DeFi ecosystem, where digital assets can be put to work in smart contracts to generate market-leading yields for their holders, comprises just a fraction of the ~$3 trillion digital asset market capitalization.

What’s driving the gap between market cap and protocol utility? The answer can be found somewhere at the intersection of sky high DeFi yields and the fragmented on & off-chain liquidity experience. Simply put, DeFi is missing an institutionally-focused platform that solves the trusted-counterparty problem. Institutional capital is the key to the next stage of growth on this fast moving financial frontier. The platform that solves this issue is poised to propel DeFi to the moon.

DeFi is the New Frontier for Structured Financial Products

DeFi, short for Decentralized Finance, is a compelling proposition. It represents a new financial paradigm — an updated, efficient infrastructure for the legacy database world.

In comparison with traditional capital markets (which still operate on the SWIFT network – first established in the 1970s), DeFi comprises innovative features including near-instant settlement, system resilience, transaction transparency, infinite composability (representing a sea of opportunity for the next-gen financial engineer), and distribution of ownership – otherwise known as decentralization – a key feature of these applications.

It is the financial application layer on top of blockchains made up of a set of coded programs that are known as ‘smart contracts’. These self-executing programs power the marketplaces housing the natively-digital structured financial products. With DeFi, users can, in effect, become their own banks through the apps allowing them to trade, borrow, lend and custody their own assets — in the name of prosperity and democracy. However, in order for DeFi to fulfill its promise of revolutionizing capital markets and the economy as we know it today, liquidity is needed. Lots of it.

Liquidity is the lifeblood of all markets. Moreover, efficient liquidity is particularly important for financial markets, which underpin the world as we know it today. It’s for this reason that the prospect of DeFi is so inspiring and intriguing, yet threatening. Infinitely composable, accessible, and interoperable capital flows (‘money legos’) are the key to financial revolution.

In order to achieve this aspirational ‘money legos’ fluidity, DeFi needs to be accessible to everyone. Currently, one majorly important stakeholder group is still sitting on the sidelines: institutions, the gatekeepers of the world’s capital flows. The tides are a-changin’ and these capital flows are itching to make their way into the DeFi arena, but a key problem needs to be solved first.

Large institutions custodying hundreds of millions of dollars – like banks and pension funds – have to fulfil internal risk requirements, including suitable KYC and AML measures. They may be able to hold Ether or derivatives of digital assets, but they are still ‘blocked’ from putting that capital to work in the majority of today’s DeFi protocols. So whilst high net worth individuals and accredited investors can transact autonomously and use DeFi in a permissionless, open and trustless manner, traditional institutions are compelled to sit on the sidelines.

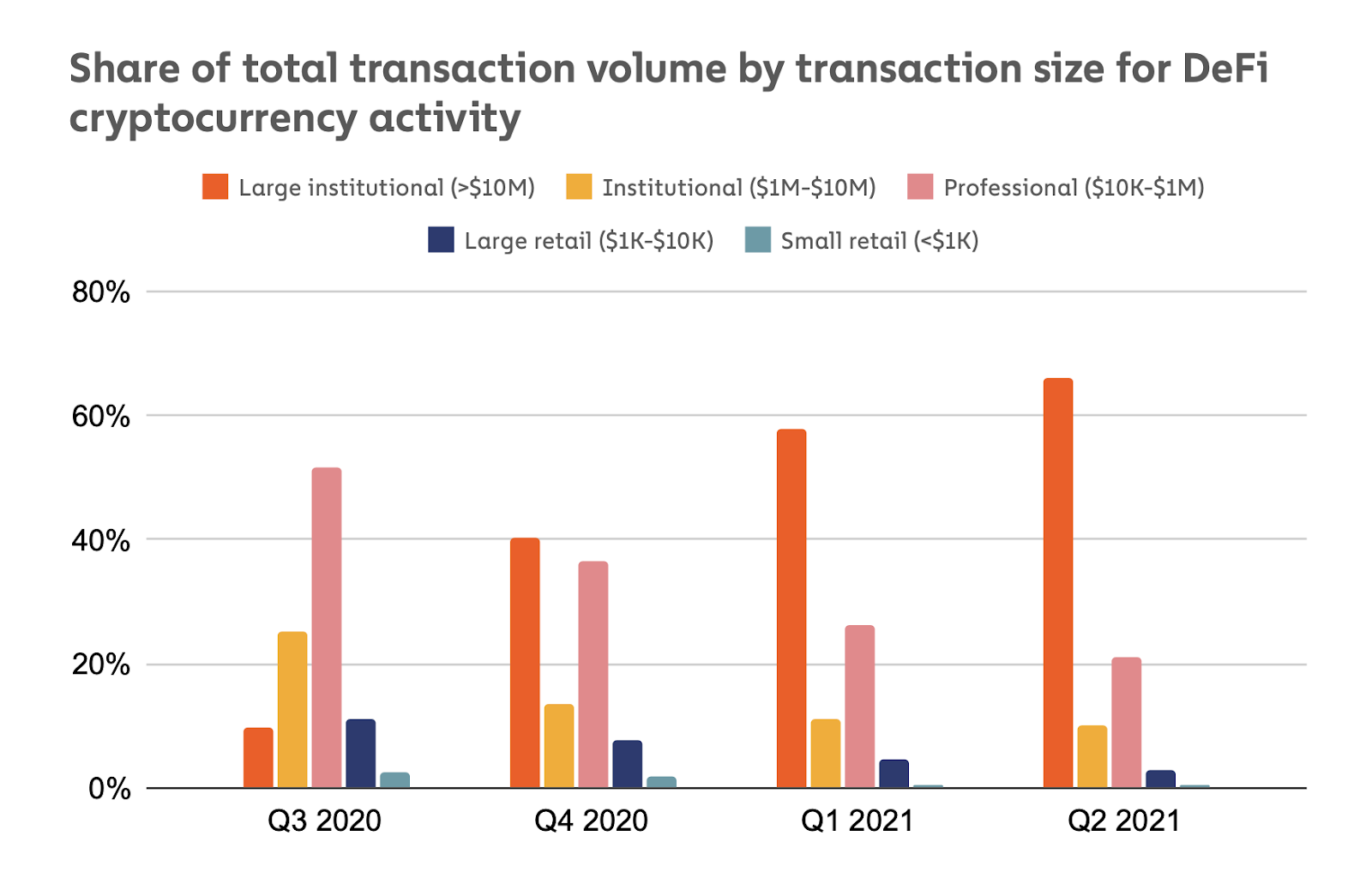

Currently, the largest transactions driving 60% of total traffic in DeFi are over $10 million in value [Chainalysis]. These are conducted by the crypto insiders with large balances of digital assets like Ether allocated to the smart-contract protocols…

… but imagine if the Blackrocks and Vanguards of the world could access the decentralized financial ecosystem. What’s missing is the launchpad for these types of players … an on-chain platform that encapsulates the DeFi ethos, while providing a trusted-counterparty, institution-grade experience. A platform like this is needed to serve the cautiously investing, principal protection focused family offices, asset managers and banks. More specifically, a KYC/AML compliant platform with an emphasis on risk management and control, poised to unleash the tide of institutional capital to flow on-chain is required. Institutional DeFi.

Protocols like our own (at Alkemi Network) have built the technology for users to participate in DeFi, integrating a KYC/AML layer into the liquidity network to mitigate some of the broader risks and anticipate institutional requirements. The vision: enable a gradual, safe and carefully-considered migration from centralized financial infrastructure to the emerging on-chain ecosystem.

By integrating additional onramps for centralized exchanges, trading platforms and neobanks to plug into a KYC/AML-approved DeFi network with one-click functionality, it is possible to accelerate mainstream CeFi adoption. On the borrowing side, protocols such as Aave are already modelling ways for users to achieve 99% Loan-to-Value but the next step is to facilitate undercollateralized loans similar to traditional financial markets; this is a reality within the Institutional DeFi framework.

Risks including smart contract exploits and scams are also mitigated by the combination of allow-listing and the inherent transparency of blockchain transactions, especially on an institution-grade settlement layer like Ethereum. Gas prices of a couple of hundred dollars are also not a great concern when the consideration of a transaction is $10 million; in fact, compared to traditional financial transaction costs, it’s negligible.

So where to from here? The key is to fuel adoption without constraining innovation. The inherent composability of DeFi will lead to a wealth of financial utility although that will inevitably bring more complexity, further raising the barrier to entry for newcomers.

To lower the barrier, we need more bridges connecting the old school to the new, that can deliver the traditional finance platforms into the decentralized financial ecosystem. With more movement across platforms, we also need better standards to ensure efficiency and security, as well as innovations that bring off-chain data on-chain. These will serve users, platforms, and will ultimately reduce the need for top-down intervention by regulators. Identity and trust underpin human activity and there is significant opportunity to harness the features of Web3 functionality to capitalize on this new frontier of financial markets.

Alkemi Network ($ALK) unlocks professional DeFi for financial institutions via its money market lending pools (built on Ethereum). With an emphasis on trusted counterparty liquidity, the protocol solves the capital, control, and connectivity problem currently preventing CeFi from entering DeFi. Learn more at docs.alkemi.network and apply for Alkemi Earn pool access directly via kyc.alkemi.network.

Brian Mahoney

Brian Mahoney is the Co-Founder and Chief Strategy Officer of <a href="https://www.linkedin.com/company/alkeminetwork/">Alkemi</a>. Alkemi Network is an institution-grade liquidity network facilitating professional DeFi for financial institutions and individuals to earn yields on their Ethereum-based digital assets. Through its institution-grade protocols and trusted-counterparty environment, the Network unlocks compliant access to decentralized markets. <section id="1459506637" class="pv-profile-section__card-item-v2 pv-profile-section pv-position-entity ember-view"> <div class="display-flex justify-space-between full-width"></div> </section>