USDT+0.01%

Crypto

USDT+0.01%

Crypto

Curve 3pool Returns to Parity After USDT Regains Dollar Peg

USDT defies all rumors and survives extreme market conditions.

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

Summer’s crypto contagion seems to have lost all steam. After a major imbalance post-Terra meltdown, Curve’s liquidity 3pool ratios have stabilized between DAI, USDC, and USDT stablecoins.

Immediately after Terra’s UST stablecoin crashed, on May 11th, there was a frenzy to acquire Tether (USDT), reaching 83.4% share in the DAI/USDC/USDT pool. In uncertain times, this is typical as people look for assets that have a long track record for stability.

At the end of July, Curve’s 3pool basket of stablecoins returned to normal, with USDT making 23.4% of the share. Because DAI is partly collateralized by ETH, which also depreciated in price, it suffered the largest contraction in May.

It also appears that Tether’s (USDT) cash reserve concerns were unfounded, having gone into the green USD peg zone, at above 1:1. During multiple crypto bankruptcies and insolvencies, many have wondered if Tether’s redeemability is secure.

Stablecoins: Closed Contagion Loop

Just prior to May’s crash, TerraUSD (UST) became the third largest stablecoin by market cap, at $18.78 billion. However, because it was an algorithmic stablecoin reliant on the price of Terra (LUNA), it collapsed overnight once the market turned bearish and suppressed LUNA. In a classic bank run, investors started to exit their positions in droves to greener stablecoin pastures.

As the oldest and largest stablecoin by market cap, USDT was the first choice, providing a redeemable pool of $83.17 billion a day before Terra collapsed. Under the redemption wave, USDT’s peg wobbled by losing -46%, spooking the market further. Nearing the end of May, $10 billion worth of USDT were redeemed, withstanding the first major market stress.

Since then, Tether’s market cap shrunk by -20.4%, to $66.22 billion. Because of the wobbling incident, USD Coin (USDC) gained traction, having raised its market cap by +12.2%, from $48.47 billion to $54.2 billion. In the redeemability aftermath, despite USDT’s reserve rumors, the largest stablecoin withstood all stress points.

Algorithmic Stablecoins: Failed Experiment

It also bears noting that other algorithmic stablecoins besides Terra’s UST completely failed. Compared to a minor (-0.46%) and short-lived USDT peg wobble, algorithmic Neutrino (USDN) completely collapsed.

Likewise, algorithmic Fantom USD (fUSD) and DEI (DEI) from Deus Finance failed to maintain their USD pegs, at -42% and -81% respectively. This happened despite their over-collateralization to their native tokens.

At this point, it is safe to conclude that market headwinds can easily crush algorithmic stablecoins, especially if their market caps are small.

Join our Telegram group and never miss a breaking digital asset story.

Is Tether’s Redeemability Stable?

So far, USDT withstood over $16 billion in redeemed stablecoins without meaningfully losing its peg. In fact, one USDT is now worth more than one USD, indicating that its demand is higher than supply. As extreme market conditions go, this was a successful stress test.

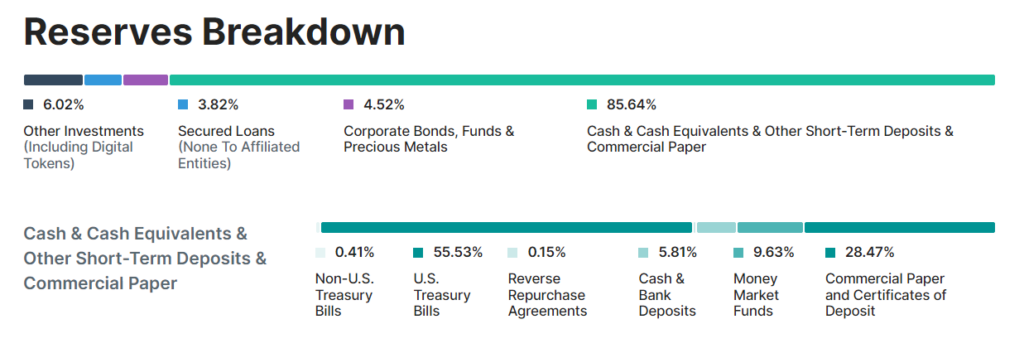

However, to be 100% backed by cash reserves, Tether has some ways to go. According to an audit published in May by Tether, it has 55.53% in US treasury bills, which is cash as we know it. The rest largely consists of commercial paper and certificates of deposit.

Since then, Tether’s most recent statement on July 27th noted they reduced commercial paper reserves to a record-low level, at $3.7 billion compared to last July’s level of $30 billion. The plan is to reduce it to zero by November 2022.

In the meantime, hedge funds shorting Tether have made the wrong bet, as shown by the continual decline in aggregated funding rate. Nonetheless, given the fact that USDC has ramped up its transparency with weekly reserve audits, Tether will have to make a similar move to not lose its stablecoin dominance.

Do you think the DeFi market will become sufficiently large and mature for algorithmic stablecoins to regain confidence? Let us know in the comments below.

Tim Fries

Tim Fries is the cofounder of The Tokenist. He has a B. Sc. in Mechanical Engineering from the University of Michigan, and an MBA from the University of Chicago Booth School of Business. Tim served as a Senior Associate on the investment team at RW Baird's US Private Equity division, and is also the co-founder of Protective Technologies Capital, an investment firm specializing in sensing, protection and control solutions.