SUI+0.36%

Market Analysis

SUI+0.36%

Market Analysis

Goldman Sachs Raises Robinhood (HOOD) Price Target to $105

Goldman Sachs Raises Robinhood Price Target to $105

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

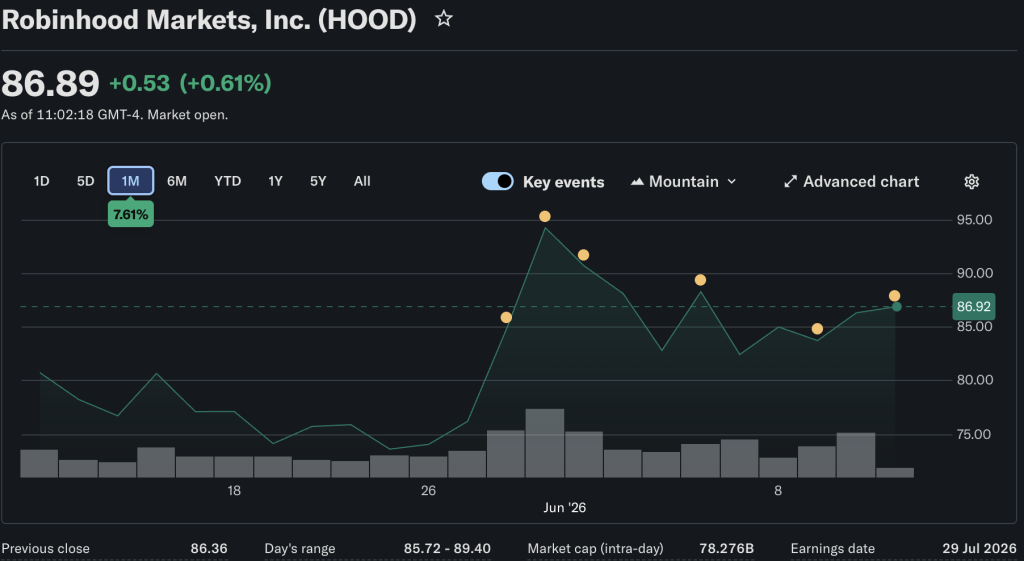

Goldman Sachs raised its price target on Robinhood Markets (NASDAQ: HOOD) from $95 to $105 on June 4, 2026, maintaining a Buy rating, implying 20.7% upside from HOOD’s prior close of $86.96.

The $10 increase, driven by Goldman analyst Will Nance, reflects the firm’s conviction that the market continues to underestimate Robinhood’s long-term earnings power across its expanding product suite. HOOD had already delivered approximately 274% returns over the prior 12 months heading into the call.

The upgrade lands as Robinhood continues its transformation from a commission-free retail brokerage into a broader financial platform, adding crypto, retirement accounts, a credit card, and international market access, a product depth that Goldman views as the structural foundation for durable monetization well beyond near-term trading volumes.

Goldman Sachs Thesis: Platform Monetization and Geographic Expansion Outweigh the Q1 Miss

Goldman Sachs has set a revised price target of $105 for Robinhood, arguing that the market is undervaluing the firm’s revenue potential. Their EPS forecasts for fiscal 2025 and 2026 are slightly above consensus, suggesting analysts may be overly conservative about Robinhood’s earnings growth.

This comes despite a slight earnings miss in Q1 2026, with Robinhood reporting EPS of $0.38 versus a $0.39 estimate and revenue of $1.07 billion versus a $1.14Bn forecast. While equity volumes fell short of Goldman’s expectations, they were higher than the Street implied, especially in options trading. However, crypto volumes underperformed significantly.

Goldman views the earnings miss as short-term noise against a backdrop of strong year-over-year revenue growth of 15.1% and solid profitability metrics. Analysts forecast full-year EPS of $1.85 for the current fiscal year, supporting a positive outlook for fintech stocks.

Robinhood’s acquisition of WonderFi opens the Canadian crypto market, and the rollout of TradePMR targets higher-value recurring revenue from registered investment advisors, further enhancing its growth thesis. Goldman believes these strategic moves are not fully reflected in the current valuation.

HOOD Stock Brief: Price Action, Valuation, and Analyst Consensus

As of June 4, 2026, HOOD shares closed at $86.96, up $4.11 on a volume of 17.8 million shares, about 40% below the 30-day average. The stock has a 52-week range of $63.51 to $153.86, with a 50-day moving average of $77.51 and a 200-day moving average of $93.34.

Robinhood’s market cap is $78.31Bn, with a trailing P/E ratio of 42.10 and a PEG ratio of 2.64. Its beta of 2.35 indicates sensitivity to retail trading and crypto cycles, important for assessing concentration risk in high-growth stocks.

Wall Street consensus includes 19 Buy, 4 Hold, and 2 Sell ratings, with a consensus price target of $106.54. Other targets range from $82 to $122, reflecting divergent views on the sustainability of Robinhood’s growth amid a competitive digital brokerage landscape.

Forward Catalysts: What the Goldman Call Needs to Stay on Track

Goldman Sachs upcoming earnings report will be crucial in assessing their revised thesis, with a focus on crypto volume recovery, options take-rate trends, and international subscriber growth to meet the $1.85 EPS forecast.

A rebound in crypto activity, HOOD’s highest-margin segment, would support the $105 target. On the institutional front, Norges Bank’s new $1.20Bn position and director Meyer Malka’s purchase of 181,000 shares for $15.1M signal confidence.

This, despite $40.2M in insider sales recently. The stance of other Wall Street firms will influence consensus pressure on the stock in the coming quarters.

The author does not hold or have a position in any securities discussed in the article. All stock prices were quoted at the time of writing.

Tim Baker

Tim Baker is a Senior Market Analyst at Tokenist with over a decade of experience educating readers about traditional finance, crypto and DeFi. A former equity researcher turned on-chain analyst, Tim specializes in regulatory framework shifts and institutional DeFi adoption. His work focuses on distilling complex liquidity cycles and the macro environment into actionable intelligence for the modern DIY investor.