BTC+4.86%

Market Analysis

BTC+4.86%

Market Analysis

Tesla (TSLA) Rallies +6.3% on Robotaxi Launch News

Tesla Rallies 6.3% on Robotaxi Optimism: Can FSD Offset Margins?

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

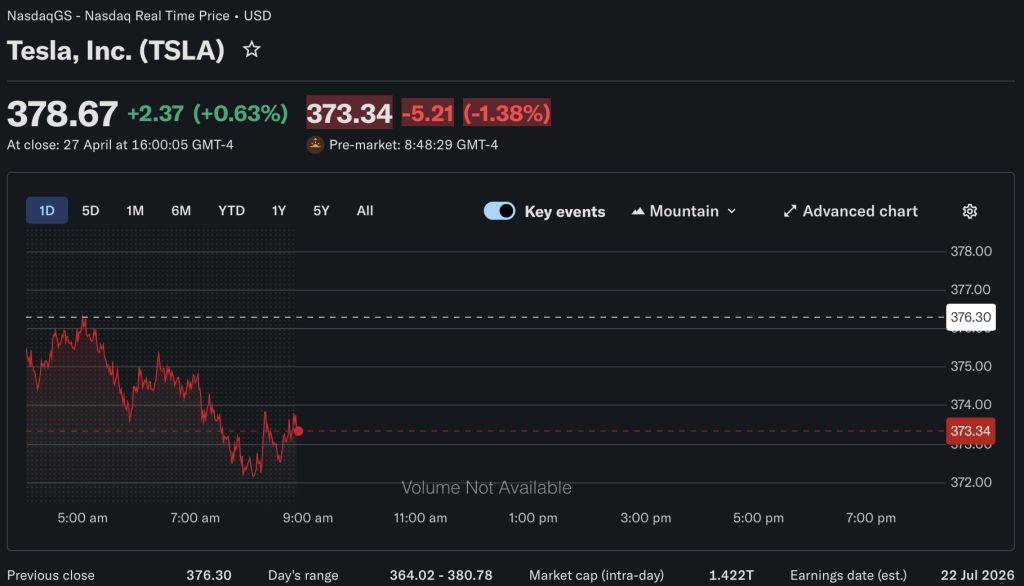

Tesla, Inc. (NASDAQ: TSLA) added $2.37 per share to close at $378.67 on Monday, a 0.63% gain, as investor sentiment pivoted toward the company’s autonomous-driving roadmap and a dedicated robotaxi unveiling event scheduled for later in 2026.

The move pushed Tesla’s market capitalization above $1.2 trillion, keeping it among the world’s most valuable companies despite a post-session pullback to $375.64 in today’s (April 28) trading session.

The rally is less about what Tesla delivered last quarter and more about what investors are willing to pay for what it might deploy over the next 4 to 8 quarters.

The central question is whether accelerating FSD revenue and a viable robotaxi network can structurally offset the automotive margin compression that has defined the past several earnings cycles – a debate that sharpens considerably ahead of each Tesla earnings report.

Robotaxi Optimism Collides With Documented Margin Headwinds for TSLA

Tesla’s planned 2026 robotaxi launch is driving investor interest, with Elon Musk promoting it as a revenue-generating autonomous vehicle. Regulatory progress in California and Texas, along with improvements in FSD version 13, have made this event appear credible. Analysts like Dan Ives view the autonomous mobility opportunity as transformative, while Morgan Stanley cites robotaxi deployment as vital for valuation.

However, Tesla faces challenges, including pressure on automotive margins due to competition from BYD and European EVs. Q1 2024 automotive gross margins fell to 16.4%, and U.S. vehicle sales dropped 23% in November 2025, with China also seeing its first annual sales decline. Additionally, the investment required for FSD and robotaxi infrastructure puts cash flow under pressure.

Meanwhile, production of the Cybertruck is ramping up at the Texas Gigafactory, and the Megapack energy storage business is thriving, but these segments alone aren’t enough to significantly shift Tesla’s cost structure. This is why the FSD and robotaxi plans are critical to the stock’s valuation.

The FSD Revenue Equation: Bull Case vs. Execution Risk

The bull case for Tesla hinges on the potential for Full Self-Driving (FSD) to evolve into the core of a robotaxi fleet, transforming revenue from low-multiple automotive manufacturing to high-multiple AI services.

Conversely, the bear case emphasizes execution risks and competition. Waymo already completed 14 million robotaxi rides in 2025, establishing a revenue-generating service that Tesla has yet to match.

Morningstar has called TSLA overvalued ahead of Q4 2025 earnings, suggesting that a full rollout may not happen until 2027 or 2028, while California’s regulation of FSD adds further risk. Moreover, Tesla will face competition from companies like Nvidia and Uber, complicating its market entry.

Morgan Stanley has downgraded Tesla to Hold with a $425 target, citing valuation issues that are not aligned with automotive fundamentals. This tension between the promising AI narrative and current margin realities poses challenges for investors.

TSLA Stock Brief: Price, Analyst Targets, and Key Metrics

Tesla, Inc. (NASDAQ: TSLA) closed at $378.67 on Monday, up 0.63%, before slightly declining to $377.87 in after-hours trading. The stock’s 52-week range is $138.80 to $479.86, highlighting its volatility due to delivery cycles and news on margins and autonomous driving. With a market cap of over $1.2 trillion, Tesla remains a key player in the S&P 500 and Nasdaq-100.

Analyst targets vary significantly: Wedbush’s Dan Ives targets $600 (Buy rating) based on a 2026 autonomy ramp, while Morgan Stanley downgraded to Hold at $425, citing high valuations.

The consensus target ranges from $380 to $420. Tesla’s high forward P/E reflects expectations for future software and autonomy revenue, which have yet to be proven.

Geopolitical risks, including cyber threats, could impact operations. Investors will focus on the August 2026 robotaxi unveiling for key updates on FSD metrics, new city expansions, and automotive margins, which will influence TSLA’s ability to maintain its premium valuation.

None of the authors of this article holds positions in TSLA or any securities mentioned. Price quotes reflect available data at the time of writing and may not reflect real-time market prices. This article is for informational purposes only.

Tim Baker

Tim Baker is a Senior Market Analyst at Tokenist with over a decade of experience educating readers about traditional finance, crypto and DeFi. A former equity researcher turned on-chain analyst, Tim specializes in regulatory framework shifts and institutional DeFi adoption. His work focuses on distilling complex liquidity cycles and the macro environment into actionable intelligence for the modern DIY investor.