TSLA Q1 Moment of Truth: Can AI Promises Mask Growing Issues?

Tesla Q1 2026 Earnings: Can AI Justify $10B+ Capex Spend?

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

Tesla, Inc. (NASDAQ: TSLA) is set to report Q1 2026 earnings after the market close today, April 22, with analysts and investors focused less on delivery figures and more on whether Elon Musk can justify a $20+ billion AI infrastructure spending plan against a backdrop of tightening automotive margins and negative free cash flow.

The company’s $1.5 trillion market capitalization rests heavily on the promise of autonomous driving at scale, a promise that Wednesday’s call must begin to quantify or face growing investor skepticism.

Tesla Earnings Preview: The $20Bn AI Capex Question

Tesla plans to invest over $20Bn in autonomous driving, AI, and robotics, sparking debate on Wall Street. Despite doubling capital expenditures (capex) year over year, the company is facing negative free cash flow, raising investor concerns about its valuation and declining EV demand.

Morgan Stanley noted Tesla’s achievement of 10 million miles driven on its Full Self-Driving (FSD) program as a sign of leadership but stressed the need for clearer progress in autonomy to support its stock price. A significant portion of the capex is directed toward Dojo, Tesla’s AI supercomputer, but its impact on autonomy remains unclear.

CFRA Research analyst Garrett Nelson highlighted the need for quantifiable returns from these investments and called for greater transparency.

Furthermore, the slow progress on the robotaxi program and growing competition, such as Nvidia’s partnership with Uber, are putting pressure on Tesla to clarify its plans in upcoming communications, particularly regarding FSD commercialization and the robotaxi roadmap.

Delivery Rebound Provides Limited Cover for Margin and Inventory Concerns

Analysts project Tesla will report a +10.8% revenue increase to $21.4Bn, recovering from a year affected by sales challenges related to Elon Musk’s political activities.

Tesla’s Q1 auto deliveries rose +6.3% to 358,023 units, but JPMorgan Chase noted that production exceeded deliveries, resulting in the largest inventory build in Tesla’s history.

This surplus may indicate weakening demand or a production strategy tied to new models, which could negatively impact margins. Automotive margins have faced pressure since Tesla began a global price-cutting cycle in 2023.

While Tesla’s energy storage segment continues to grow, it hasn’t yet compensated for the vehicle business’s difficulties. Unlike other tech firms monetizing AI investments, Tesla’s path hinges on the deployment of autonomous driving technology, which Musk has delayed, raising questions about its impact on future margins.

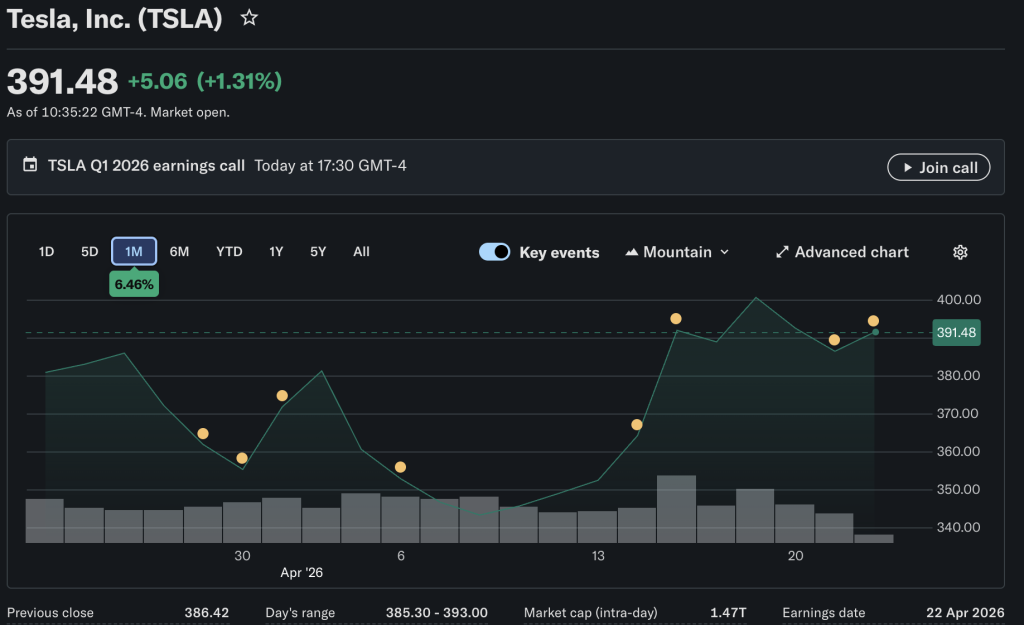

TSLA Stock Brief: Price, Analyst Targets, and Key Metrics

TSLA closed Tuesday at around $385, giving it a market cap of roughly $1.5 trillion. Wedbush’s Dan Ives has a $600 price target, suggesting over 55% upside, viewing the upcoming earnings call as crucial for the AI narrative. Conversely, JPMorgan Chase believes TSLA is overvalued due to its capital-intensive roadmap and negative free cash flow, highlighting a significant divide among analysts.

As of Q1 2025, Tesla held $37Bn in cash, offering a liquidity buffer amidst rising capex. However, the company’s capacity to fund its AI goals without dilution or debt raises concerns. Unlike peers that have initiated buybacks or dividends, Tesla’s investment case hinges on achieving milestones in autonomous driving.

The stock’s 52-week range is from $138 to $480, reflecting sensitivity to Musk-related sentiment and EV demand. TSLA has underperformed the S&P 500 this year, though it has recovered from its 2026 lows amid renewed optimism in autonomous driving.

The options market anticipates significant volatility post-earnings, with analyst targets varying widely. The earnings call’s insights on Dojo scaling and FSD commercialization will be critical in determining TSLA’s valuation and outlook for the second quarter.

None of the authors of this article holds positions in TSLA or any securities mentioned. Price quotes reflect available data at the time of writing and may not reflect real-time market prices. This article is for informational purposes only.

Tim Baker

Tim Baker is a Senior Market Analyst at Tokenist with over a decade of experience educating readers about traditional finance, crypto and DeFi. A former equity researcher turned on-chain analyst, Tim specializes in regulatory framework shifts and institutional DeFi adoption. His work focuses on distilling complex liquidity cycles and the macro environment into actionable intelligence for the modern DIY investor.