BTC-0.25%

Market Analysis

BTC-0.25%

Market Analysis

Is MSTR Stock Still a Buy as it Builds a Massive Bitcoin Pile?

There is a difference between risk diversification and enforced decentralization.

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

On Friday, Michael Saylor’s MicroStrategy acquired another batch of bitcoins. This time, MicroStrategy’s Bitcoin reserves increased by 7,420 BTC bought at $458.2 million, or ~$61,740 per BTC. This puts the company’s Bitcoin holdings at a total of 252,220 BTC, worth nearly $10 billion at an average price of $39,266 per BTC.

Year-to-date, Bitcoin gained 42% value, presently priced at $62,875, which is already above MicroStrategy’s latest acquisition price. In the same period, MSTR stock gained 110% in value. As a clear proxy to Bitcoin exposure, investors see MicroStrategy as a leveraged fee-less option instead of having to tackle the self-custodial risk of direct BTC ownership.

Having delegated this responsibility to MicroStrategy, does that mean that MSTR ownership is preferable to holding Bitcoin itself in the long run?

How Does MicroStrategy’s Debt Leveraging Work?

Just like before, MicroStrategy bought the latest batch of bitcoins using the debt instrument of convertible notes. As a form of debt, convertible notes incur interest rate and maturity date, but they also offer conversion to equity ownership. This way, investors are betting on a future return on investment, rewarding them with a discounted stock price.

This time, MicroStrategy finished the private issuance of $1.01 billion in Convertible Senior Notes, first announced on Monday at a more modest range of $700 million. Under the Rule 144A of the Securities Act of 1933, MicroStrategy incurred on itself an obligation to pay 0.625% annual interest, starting from March 15, 2025 and finishing on maturity date on September 15, 2028.

MSTR stock is presently priced at $145.16, but with the conversion price of $183.19, accounting for principal and accrued interest, MSTR shareholders would be up for a 26% premium. Of the completed $1.01 billion convertible senior notes sold, $135 million of which was allocated as an extra option to buy notes within 13 days from when they were first sold.

MicroStrategy’ Gambit: Buying Scarcity with Eroding Currency

Bitcoin plays a perfect role for such a strategy as a scarce resource, limited to 21 million BTC and enforced by a network of Bitcoin miners that use enormous energy and hardware assets to secure Bitcoin’s inviolability.

This way, it is easy for investors to see Bitcoin not only as a digital asset, but one that is firmly anchored in physical reality via a proof-of-work consensus algorithm. For MSTR investors, the underlying assumption is that Bitcoin scarcity will more than offset MSTR exposure, while giving the buyers of convertible notes a premium.

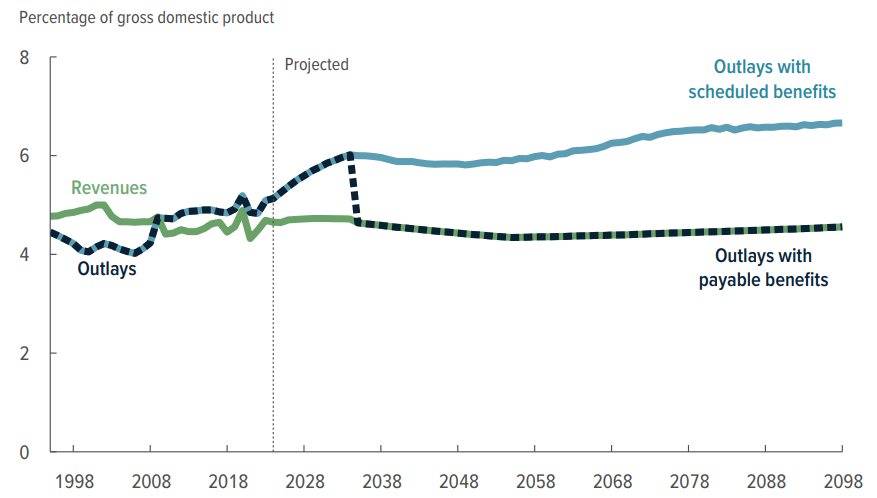

On a macroeconomic level, this thinking makes sense because it is exceedingly unlikely that USG will ever prioritize financial austerity to reduce debt over profligate spending. For social security expenditures alone, the Congressional Budget Office (CBO) projected a great bifurcation between feasible (payable) benefits and scheduled benefits, as a percentage of gross domestic product (GDP).

Likewise, USG military expenditures have relentlessly increased over the decades, having reached a record high of $876.94 billion in 2022. In other words, the Federal Reserve’s printing machine will have to be turned on. And as the Fed’s balance sheet gets bloated, the value of the dollar will decrease.

After all, the value of $1 USD in 1913 (the year the Federal Reserve was established) is $31.80 in 2024, having eroded after a 3,079% cumulative inflation rate. Essentially, MSTR shareholders are counting on the devaluation of USD.

As the value of the currency decreases, so does the real value of the debt. Moreover, the commodity hedge for that debt is Bitcoin, which holds mathematically predictable inflation and fixed scarcity, unlike gold or silver which have pseudo-scarcity.

Against Diversification to Avoid Hugo Stinnes’ Fate?

Industrialist Hugo Stinnes made exactly such a leveraged debt gambit in Weimar Germany, having purchased hard assets like factories and coal mines with rapidly devaluing German marks. Ultimately, Stinnes earned a moniker “Inflation King” with this strategy.

Although the Hugo Stinnes empire fell following the introduction of the Rentenmark in 1924, his holdings were greatly diversified. In contrast, Michael Saylor has made it clear he is against the diversification of assets, having stated in 2020 that “diversification is selling the winners to buy the losers” in an interview with Daniela Cambone.

Michael Saylor has repeated this conviction across many public appearances.

Michael Saylor on going “all in” on #Bitcoin instead of diversifying:

— Mark Harvey (@thepowerfulHRV) November 15, 2023

“How many chairs are you sitting in right now?”

H/T @Scavacini777 pic.twitter.com/1vvtqqT2lL

Although diversification is typically seen as a diversification of risk in finance, the problem with Hugo Stinnes is that his diversification was also poorly managed as he overextended into hotels, shipping, banking and newspapers.

By adopting an anti-diversification approach in the first place, Michael Saylor is eliminating that risk entirely. Even better, such a risk is replaced with a completely decentralized asset that runs on cryptographic math, enforced by computing power. In turn, this makes MSTR exposure itself as one that has a decentralized risk, despite lacking diversification per se.

Do you think MSTR investors will vindicate their confidence? Let us know in the comments below.

Disclaimer: The author does not hold or have a position in any securities discussed in the article.

Tim Fries

Tim Fries is the cofounder of The Tokenist. He has a B. Sc. in Mechanical Engineering from the University of Michigan, and an MBA from the University of Chicago Booth School of Business. Tim served as a Senior Associate on the investment team at RW Baird's US Private Equity division, and is also the co-founder of Protective Technologies Capital, an investment firm specializing in sensing, protection and control solutions.