3 “Strong Buy” Stocks to Consider Right Now

There are many times when "buy the dip" strategy backfires, but it fails less when tipped with high-profile stock buys.

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

How does one gauge the value of something? In ancient times, Roman consul Lucius Cassius coined the phrase “cui bono?”, meaning “who benefits?”. Put to modern use, when you see company executives buy their own shares in bulk, it might be a good time to mirror their actions.

Increased Accessibility in Stock Trading

Robinhood may have popularized stock trading with its commission-free trading, but other top apps for stock trading have made significant contributions to online trading as well. eToro, with its CopyTrader feature, is one of them. It allows you to circumvent a lack of in-depth stock market knowledge by copying the trades of those professional traders/insiders who have high rates of success (profit to loss ratio).

eToro markets itself as a social trading app, which means that everyone gets something out of the platform. Pro traders gain a following and get extra payouts when their trades are copied, while regular users gain access to smart trades without extra charges (only if the trades being copied use x1 leverage).

Stocks with “Strong Buy” Indicators Today

It takes a lot of time, trial & error, and social networking to hone the craft of stock market trading. If you are interested in stocks currently marked as “Strong Buy” by accomplished pro traders with insider tips, take a look at the following selection of stocks.

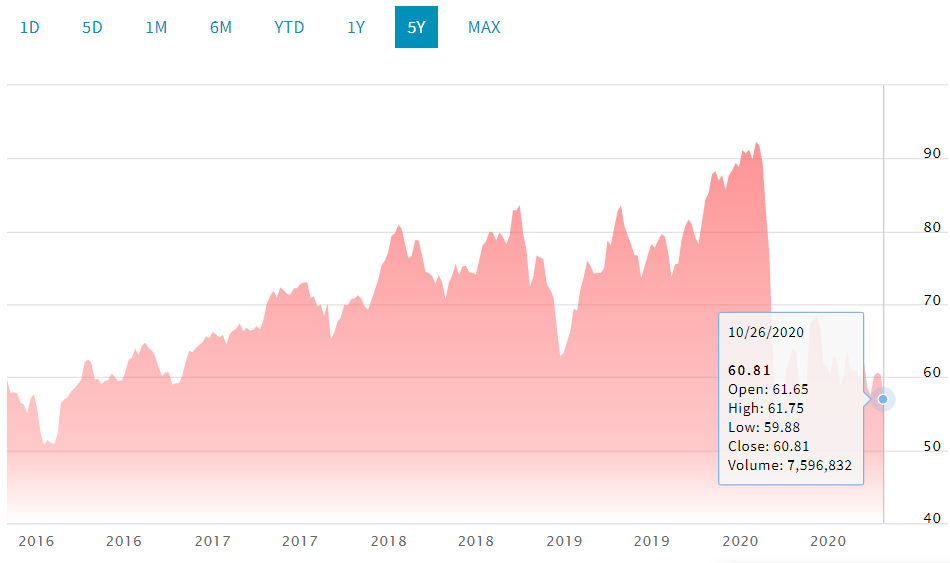

1. Raytheon Technologies (NASDAQ:RTX)

RTX Ties Fortune to U.S. Military Budget

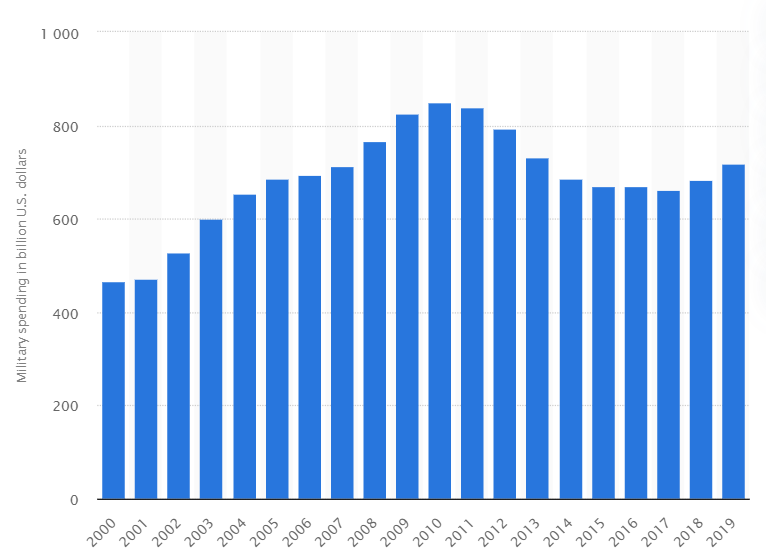

Although war is a major source of income for companies involved with supplying the military-industrial complex, there is no lack of opportunities in peacetime as well. Raytheon holds multiple avenues to thrive outside of a war footing: international weapons’ sales, research and development contracts with the Department of Defense, refitting outdated equipment, and maintenance contracts for allied nations.

As is the case with Big Tech, where digital space is dominated by few players, so is the space of Pentagon contracts reserved for companies able to provide high-end expertise and hardware. Raytheon is one of those companies. Being a key member of this exclusive club, Raytheon is in a position to draw from a massive pool of U.S. military spending.

Without starting another major war, the Trump administration has managed to keep military spending relatively high due to modernization efforts. Its highest peak was in 2010 at nearly $850 billion, as the Iraq war was winding down at the end of 2011. In 2020, military spending sits at $721.5 billion, just slightly higher than in 2019, at $718 billion.

Raytheon Executives on a RTX Stock Shopping Spree

Unfortunately for Raytheon, the pandemic fallout and lack of major military engagements had caused a revenue slump in Q1 and Q2. However, RTX ended Q3 with a recovery when EPS (earnings per share) rose by 45%, at $0.58 per share. This is in line with RTX’s two-year track record of beating quarterly earnings forecasts.

Raytheon’s dividend payouts at $0.475 per share are also holding high three quarters in a row. Its dividend yield sits at 3.5%, which is almost twice the average for the Industrial Goods space. Looking at more positive signs, Raytheon CEO Gregory Hayes recently bought $3.35 million worth of RTX shares. He was soon followed by Thomas Kennedy, Raytheon’s Executive Chairman, with a purchase of nearly $1 million worth of RTX shares.

These major shows of confidence follow Ratheon’s Q3 earnings report. In it, the company demonstrated a reduction of costs, free cash flow surpassing expectations at $1.2 billion, and increased domination of the missile supply market, along with cyber and aerospace sectors. As the company adjusts to a leaner mode of operation, the current slump represents an opportunity before its expertise is called upon again, with the current growth potential at around 22%.

2. Banc of California (NASDAQ:BANC)

California may be experiencing a middle class exodus, but it still remains the most populous state with nearly 40 million residents. As one of the largest Californian banks, headquartered in Santa Ana, BANC is more than ready to serve the remainers. Currently, the bank holds $7.8 billion worth of assets and has spread across 31 branches.

Predictably, the pandemic has turned BANC’s Q1 and Q2 earnings reports into negatives. However, the Q3 earnings report shows a net positive $0.24 EPS, exceeding a $0.14 projection. Alongside better than expected EPS recovery, BANC’s revenue also rebounded to pre-corona levels, at nearly $60 million.

Following its return to normal, BANC’s CEO Jared Wolff bought $115k worth of shares on October 29. Largely depending on credit income streams, BANC remains favorable for Wells Fargo analyst Timur Braziler. He expects further earnings momentum and tangible book value (TBV) growth extrapolating from the improvement of credit lines’ delinquencies. Accordingly, he puts BANC’s growth potential at 24%.

3. Ares Capital Corporation (NASDAQ:ARCC)

Ares represents a middle-man facilitator for all business ventures in need of capital but without ready access to loans. As an asset management company, it has thus far invested in 350 businesses, accounting for a $14 billion asset portfolio. The pandemic culling of businesses significantly reduced Ares’ revenue stream, but Q3 is showing recovery.

From Q2, at $333 million revenue, Ares conclusively rebounded with a nearly 50% revenue increase, at $497 million for Q3. Although its EPS remains flatlined at $0.39, this still exceeded negative forecasts. Going forward, Ares is confident in its growth, demonstrated by the October announcement of its exceptionally high dividend yield of 11.57%. It will sit at $0.4 per share starting at the year’s end.

A recent showing of confidence in Ares’ future came from its CEO, Kipp Deveer. At the end of October, he bought $1 million worth of shares. Although ample, his “buy the dip” strategy may have been belated, as Ares’ other top executives already bought almost $1 million worth of shares two months prior.

In total, that accounts for about $1.9 million worth of confidence-inspiring share buys among Ares’ executive branch. This puts Ares stock at 12% growth potential.

With Robinhood and eToro vying for user-count supremacy among stock trading apps, which one do you find more useful? Let us know in the comments section below.

Disclosure: Tim Fries has no positions in any of the stocks mentioned, and has no plans to initiate any positions within the 72 hours following the publishing of this article. This article expresses the opinions of Tim Fries. Tokenist Media LLC has no position in any of the stocks mentioned, and does not plan to initiate any positions within 72 hours of the publishing of this article. Please consult our website policy for more information.

Tim Fries

Tim Fries is the cofounder of The Tokenist. He has a B. Sc. in Mechanical Engineering from the University of Michigan, and an MBA from the University of Chicago Booth School of Business. Tim served as a Senior Associate on the investment team at RW Baird's US Private Equity division, and is also the co-founder of Protective Technologies Capital, an investment firm specializing in sensing, protection and control solutions.