BTC-0.25%

Crypto

BTC-0.25%

Crypto

Binance Embraces Regulation to Remain top Crypto Company

Binance takes big steps toward regulatory compliance as fully licensed competitors continue to appear.

Editorial disclosureRead more

All reviews, research, news and assessments of any kind on The Tokenist are compiled using a strict editorial review process by our editorial team. Neither our writers nor our editors receive direct compensation of any kind to publish information on tokenist.com. Our company, Tokenist Media LLC, is community supported and may receive a small commission when you purchase products or services through links on our website. Click here for a full list of our partners and an in-depth explanation on how we get paid.

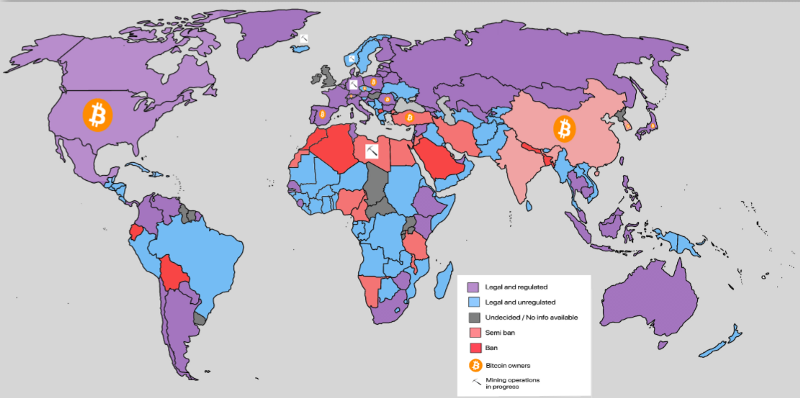

Regulations are quickly becoming the most important aspect of any company in the cryptocurrency industry. As governments around the world continue to work towards developing regulatory frameworks for crypto, companies are constantly needing to adapt to continue operating.

The world’s largest crypto exchange, Binance, has a history of ignoring financial regulations, but recently came under fire earlier this month. Now, Binance has announced that they will be taking drastic steps to better meet financial regulations.

Binance Finally Falls Into Regulatory Pressures

Binance has historically been a supporter of the anonymity digital assets provide, operating decentrally and requiring minimal KYC when users sign up for an account. To achieve basic verification on Binance, a user only needs to enter a name, an email, and a physical address. This information is not checked with any government database, giving users the ability to completely make up all the information. With just this basic information, users can withdraw up to 2 bitcoin every 24 hours.

In an official announcement, Binance notified customers that the withdrawal limit for users with basic verification will drop to 0.6 bitcoin in mid-August. This is in an effort to prevent money laundering and curb broader criminal activities happening through the platform.

Additionally, Binance CEO Changpeng Zhao (CZ) claimed that the company wants to become fully compliant and licensed in all countries it operates in. After coming under regulatory scrutiny from various countries including the US, UK, Hong Kong, Italy, Japan, and Germany among others, the company is now directing efforts towards obtaining full licensing. This comes just a few weeks after Binance declared that they are doubling the size of their compliance team.

Altogether, Binance is finally taking serious steps to be compliant around the world. After receiving various allegations and undergoing large investigations, Binance will now aid in institutionalizing and centralizing digital assets. While this goes against what cryptocurrencies stand for, it is necessary for Binance to stay relevant in many countries.

Fully Compliant Institutions Enter Crypto Space

Digital assets are now widely available for purchases on major platforms such as PayPal, Robinhood, and Coinbase—even Mastercard has started supporting crypto startups recently. As these large, fully licensed financial institutions have been expanding their crypto services, Binance is becoming less necessary for crypto investors. In order for Binance to avoid being rolled by these new players on the crypto scene, it is essential for them to up their regulatory efforts.

Even Though crypto is aimed to be anonymous, governments are finding ways to centralize crypto through regulating trading, holding, and exchanging.

With governments’ newfound control over many inexperienced crypto investors, non-compliant companies such as Binance may see a loss in business. For Binance to continue operating in many countries, it is important for them to push forward on the path towards full compliance.

Binance has been and continues to be a huge player in the crypto industry, but has had a bumpy history of legal problems. Now the exchange is making progress toward complying with government laws. How will this change impact Binance’s customer base? Will this regulation save Binance from being overtaken by licensed financial corporations? Let us know in the comments.

Charlie Perkins

<p class="p1">Charlie has been actively researching and investing in both traditional and crypto opportunities for several years. Growing up in San Francisco, he has always been fascinated by the disruptive FinTech industry. He is currently completing a degree in Business Information Systems with minors in Computer Science and Data Science from Lehigh University. Charlie has experience working for crypto startups, as well as analyzing and developing various DeFi projects. He also has comprehensive financial knowledge, completing the investment fundamentals course through The CFA Institute in 2020. When away from his keyboard, Charlie enjoys surfing and spending time with good friends.</p>